Antimony Shock: Why Prices Just 27x’d in Sixty Days

Antimony went from $1,400 per metric ton in July 2024 to $38,000 per metric ton by mid-September. That is not a price move. That is a market structure change. If you buy antimony oxide for flame retardants, antimony t…

Antimony went from $1,400 per metric ton in July 2024 to $38,000 per metric ton by mid-September. That is not a price move. That is a market structure change. If you buy antimony oxide for flame retardants, antimony trioxide for PVC stabilisers, or antimony concentrate for lead-acid batteries, the contract you signed in May 2024 no longer means what it meant when you signed it. This is what happened, why the price will not snap back, and how to rebuild your antimony supply book around it.

What changed on 14 August and 15 September 2024

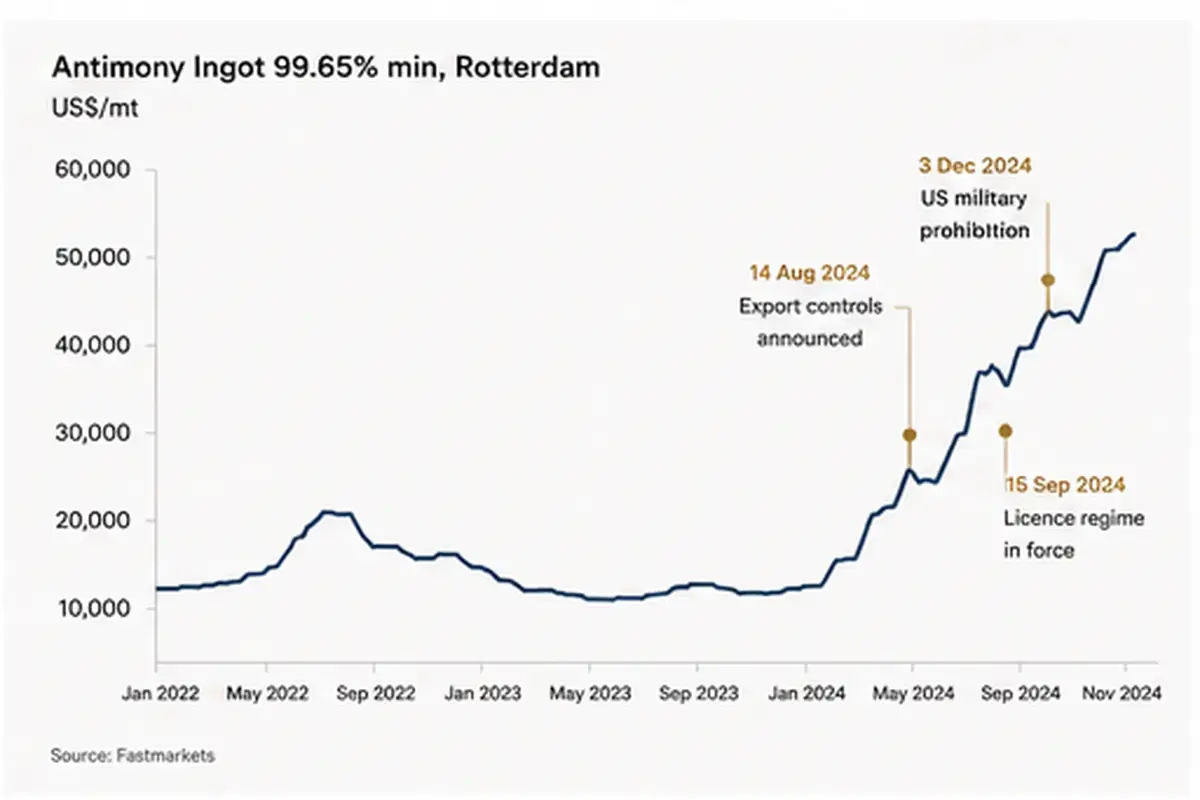

On 14 August 2024, China’s Ministry of Commerce (MOFCOM) and the General Administration of Customs published Announcement No. 33: antimony and a range of antimony compounds were added to China’s dual-use items export control list. The licence regime took effect on 15 September 2024. From that date, any Chinese exporter of antimony or antimony products had to obtain individual export licences from MOFCOM, with end-user disclosure, end-use justification, and supporting documentation.

On 3 December 2024, MOFCOM tightened the screw a second time: a full prohibition on exports of antimony products to United States military end-users, or for military end-uses.

The mechanism reads like a licensing regime. The practical effect has been a near-total halt in Chinese antimony export flow. Chinese antimony exports for September 2024 fell by approximately 97% year-on-year. October and November showed marginal recovery. MOFCOM has approved very few applications publicly. The Chinese authorities have not articulated criteria.

Why this is a structural problem, not a price spike

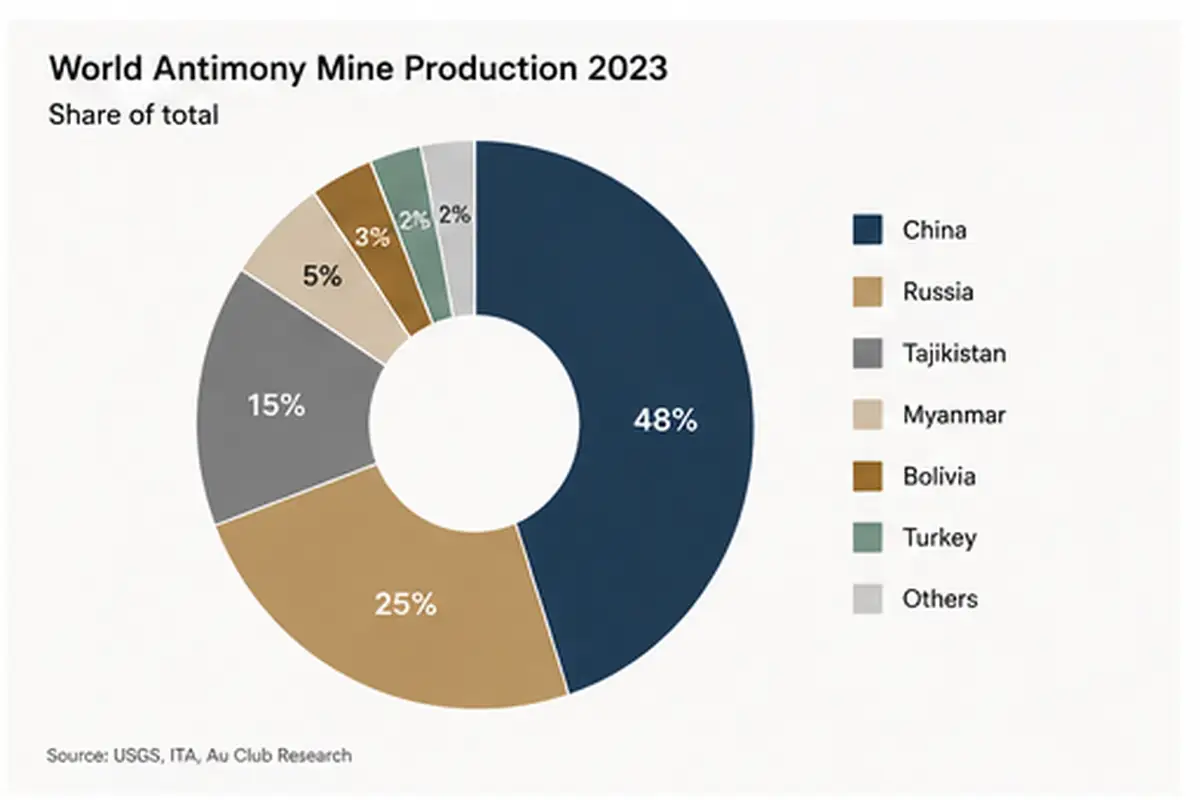

Antimony is mined in fewer than fifteen countries at commercial scale. China accounts for roughly 48% of world mine production. Russia is next at around 25%. Tajikistan is third at approximately 15%. Bolivia, Myanmar, Turkey, Australia and a handful of others make up the balance.

China’s dominance is amplified at the refining stage. Chinese smelters refine not only Chinese ore but also Russian, Burmese, and Tajik concentrate. The world’s tradeable antimony — antimony metal, antimony trioxide, antimony tri-sulphide — has moved through Chinese smelters even when the ore itself originated elsewhere.

This is why the price went where it did. The market did not just lose 48% of supply. It lost the refining and trading infrastructure that aggregated the other 52%.

Antimony price path, July–November 2024

Month | Price (USD/MT, FOB Asia) | Move |

July 2024 | $1,400 | Base |

August 2024 | $22,000 | First licence rumour priced in |

Mid-September 2024 | $38,000 | Licence regime in force |

October 2024 | $44,500 | Stocks drawn |

November 2024 | $48,000 | Spot in Rotterdam |

By early 2025 the metal traded at $51,500 per metric ton. Fastmarkets has been assessing antimony prices since the 1980s. It has never seen this kind of move.

Where antimony is consumed — and why substitution is harder than it sounds

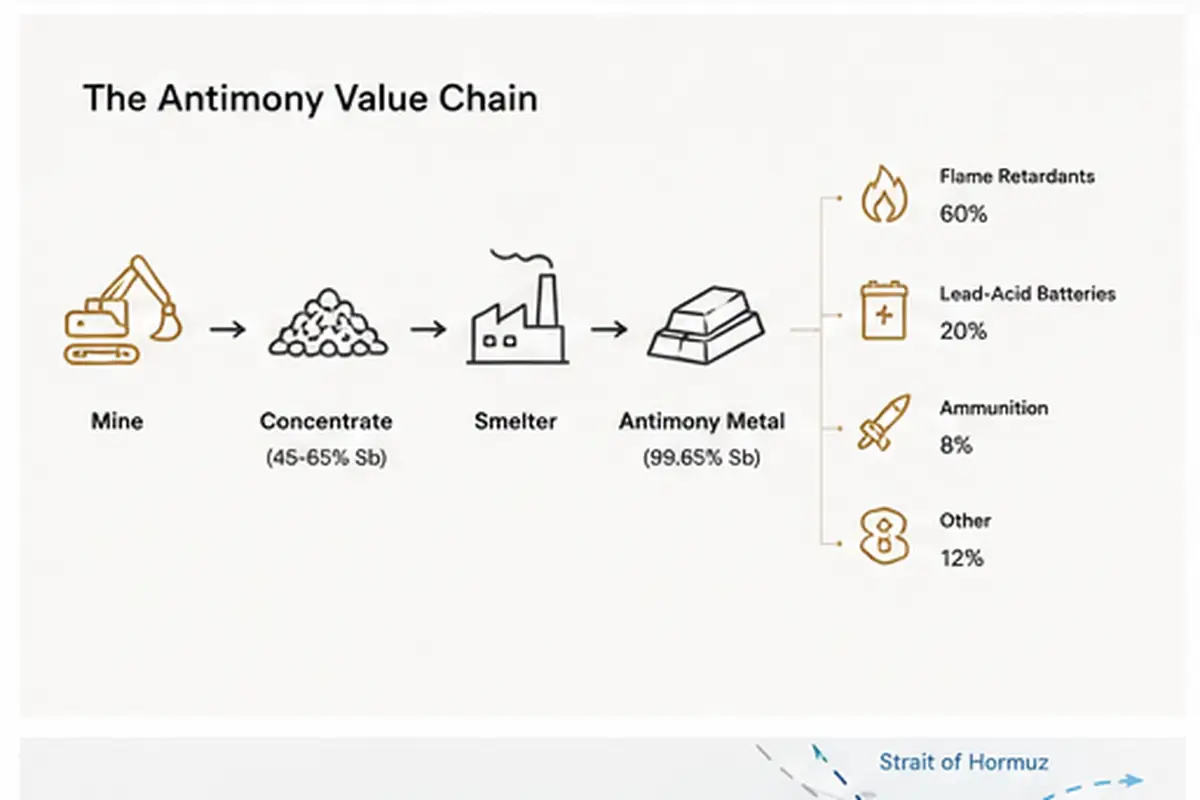

Around 60% of refined antimony goes into flame retardants — chiefly antimony trioxide (Sb₂O₃) used in PVC, ABS, polyester resins, electronics housings, electrical cable jacketing, and textile back-coatings. Approximately 20% goes into lead-acid batteries, where antimony is alloyed with lead to harden battery plates. The remainder is split between ammunition primers, glass fining, catalysts, and a small but strategically important share in solar photovoltaic glass.

Substitutes exist for some applications:

- Flame retardants — phosphorus-based and halogen-free alternatives can substitute in some polymer systems, but reformulation requires UL recertification, supplier audits, and a six-to-twelve month qualification cycle.

- Lead-acid batteries — calcium-alloyed plates already dominate the starter-battery market, but deep-cycle and stationary applications still rely on antimonial lead.

- Ammunition — no commercially viable substitute exists for antimony in primer compositions and shot hardening.

The result: industrial flame retardant buyers cannot meaningfully reduce their antimony exposure inside a twelve-month window. Battery manufacturers can only partially. The defence supply chain has no substitute path at all. That is why the December 2024 military-end-use prohibition matters — it forces Western defence procurement to find non-Chinese, non-Russian antimony at a moment when neither is reliably available.

The non-China supply map

Au Club’s working view of the non-China antimony supply universe in late 2024:

- Tajikistan — the Anzob mine and Konimansur deposit. Output is captive to Russian-aligned offtakers in practice. Commercial availability for Western buyers is limited and the routing complexity is high.

- Russia — Polyus and other producers. Sanctioned for direct sale into the US and UK markets after April 2024. Triangulation possible through third countries but creates origin documentation risk.

- Bolivia — small-scale producers. Sb concentrate of 45-60% Sb is the working grade. Logistics through Arica, Chile or the Pacific via Iquique. Volumes are small relative to demand but the origin is clean.

- Myanmar — informal mining and smelting. Significant volume historically flowed into Chinese refineries. Direct export to non-Chinese buyers exists but quality and documentation are inconsistent.

- Turkey — small mine production. Domestic consumption absorbs most of it.

- Australia — Hillgrove (NSW) restarted production planning. First commercial concentrate flow expected late 2025 / early 2026.

Au Club’s offer covers antimony concentrate (45–65% Sb) and antimony ingots, with 100-300 MT/month availability through non-Chinese routes. We do not handle Russian-origin material.

How to write a 2025 antimony contract

If your existing contracts use Fastmarkets China Sb 99.65% as the benchmark, that benchmark may not have a meaningful market behind it for non-China material. Three contractual considerations matter more than they used to:

- Origin clause — explicit identification of the country of mining and country of smelting. “Non-Chinese, non-Russian origin” is the most common Western buyer requirement post-December 2024.

- Price formula — a floating reference against Fastmarkets Antimony Ingot 99.65% Rotterdam, with an explicit premium for confirmed origin, is now the dominant structure for non-China material.

- Force majeure — should explicitly include export licence withdrawal, host-country export quotas, and shipment delays caused by sanctions screening. Generic FM language drafted before August 2024 is not sufficient.

Pre-shipment inspection should be by SGS, Alex Stewart, or Intertek with a Certificate of Analysis covering Sb, As, Pb, Bi and S content. The COA, the certificate of origin, and the bill of lading should travel as a single document set under any LC.

Au Club’s read for 2025 and 2026

The licence regime is not going to be quietly lifted. Antimony’s pricing in 2025 will be set by the cleared-licence flow from China — likely small, unpredictable, and bid-up by defence buyers — against rising non-China supply from Tajikistan, Bolivia, and eventually Hillgrove. Our working range for Fastmarkets Antimony Ingot 99.65% Rotterdam through 2025 is $42,000 to $58,000 per MT.

What we are telling buyers: lock 12-month supply now, accept a higher annual average than 2023, and structure the contract so origin documentation moves with the cargo. For 2026, plan for a market that has structurally re-priced. There is no version of this story where antimony returns to $1,400.

FAQs

Is antimony still banned from China?

Antimony is not banned. It is under a dual-use export licence regime introduced 15 September 2024. MOFCOM approves licences case by case. Export volumes since September 2024 have been a small fraction of historical levels. A specific prohibition exists, since 3 December 2024, on exports to US military end-users.

What is the antimony price today?

At time of writing in November 2024, Fastmarkets Antimony Ingot 99.65% Rotterdam was assessed around $48,000 per MT. For real-time pricing, contact our trading desk.

Where else can I buy antimony concentrate?

Tajikistan, Bolivia, Myanmar, Turkey, and (from late 2025) Australia. Au Club sources from non-Chinese, non-Russian origins and supplies 45-65% Sb concentrate plus ingots, 100-300 MT/month.

About Au Club

Au Club is a Dubai-based commodity trading company supplying marine fuel, metals, and minerals worldwide. We trade antimony concentrate and antimony ingots from non-Chinese origins, with SGS or Alex Stewart pre-shipment inspection and full documentation. To enquire about availability and pricing, contact our trading desk.