LC, SBLC, TT, DLC: A Buyer’s Guide to Commodity Trade Finance

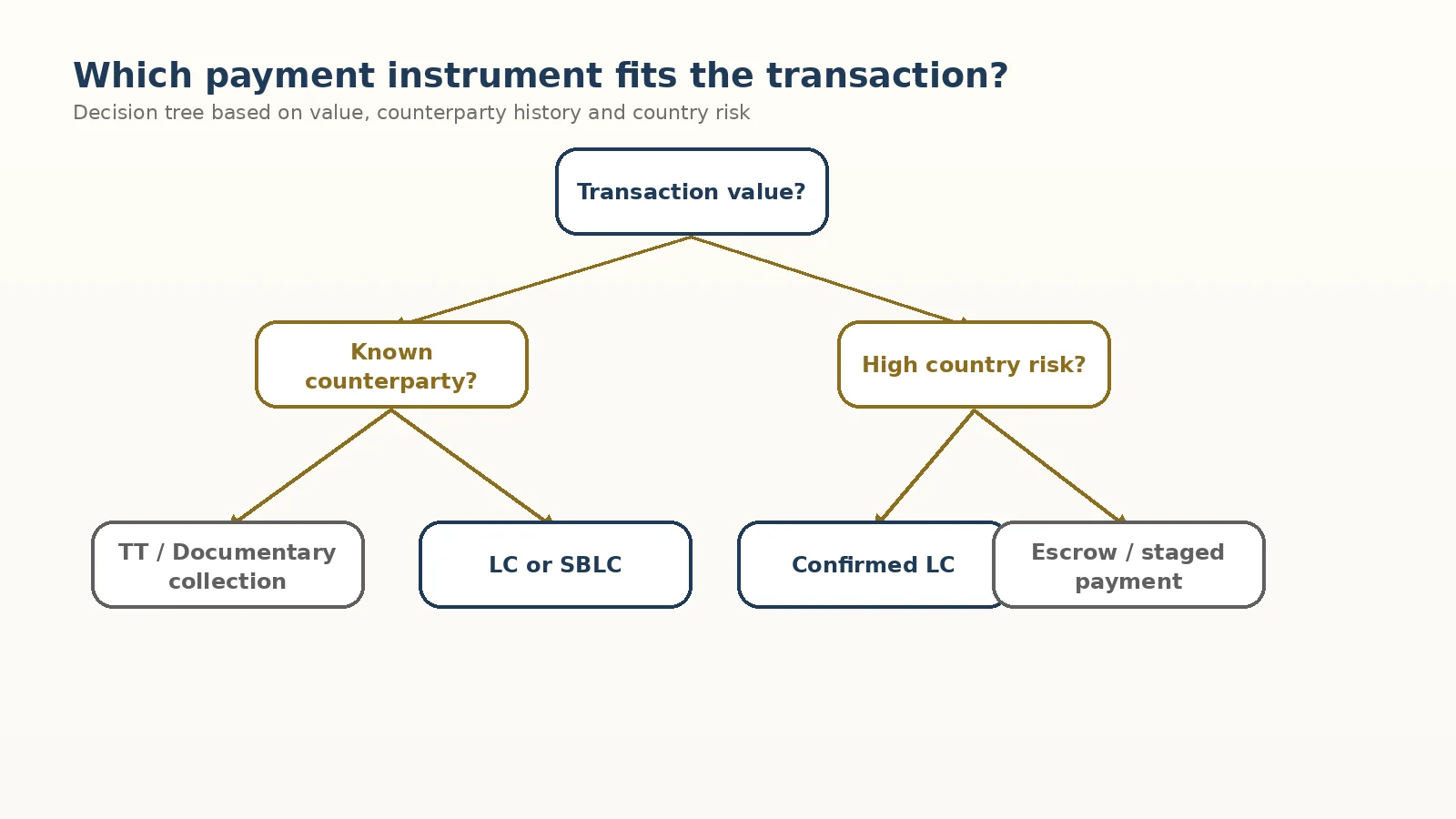

Commodity payments are not interchangeable. A confirmed irrevocable LC sits at one end of the spectrum; a 30% TT against pro-forma invoice at the other. The right instrument depends on commodity value, lead time, coun…

Commodity payments are not interchangeable. A confirmed irrevocable LC sits at one end of the spectrum; a 30% TT against pro-forma invoice at the other. The right instrument depends on commodity value, lead time, country risk, counterparty history, and bank relationships. This piece is a working trader’s plain-English reference, written for procurement teams who buy across multiple commodity categories and need to understand the trade-finance landscape without becoming bankers.

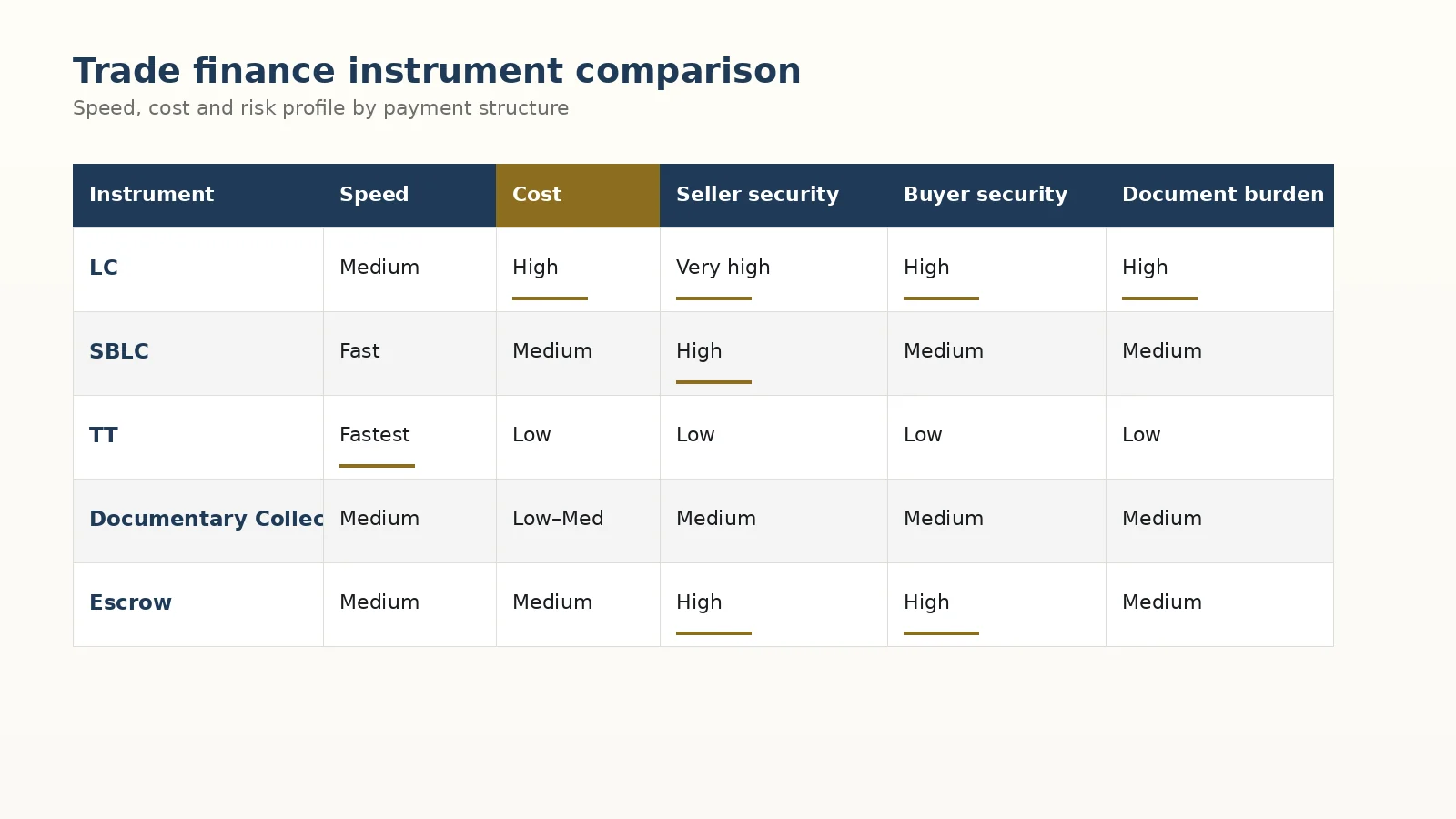

The five instruments at a glance

Five payment structures dominate commercial commodity trading:

Instrument | What it is | When you use it |

Documentary LC (DLC / LC) | Bank pays seller when seller presents specified documents | High-value cargo, unfamiliar counterparty, international trade |

Standby LC (SBLC) | Bank guarantees performance; pays only if buyer defaults | Long-term supply contracts, performance backing |

Telegraphic Transfer (TT) | Direct wire from buyer to seller | Established counterparty, lower-value transactions |

Documentary collection (D/P, D/A) | Bank facilitates document exchange against payment or acceptance | Less common in commodities but used in certain regions |

Escrow | Third party holds funds until release conditions met | New counterparty, contested transactions |

For commodity trade, LC and TT dominate. SBLC is used for long-term supply arrangements. The other instruments appear in specific scenarios.

Documentary Letter of Credit: how it actually works

The LC is the workhorse of international commodity trade. Mechanically, an LC is a bank’s promise to pay a seller a specified amount when the seller presents specified documents. The buyer (applicant) opens the LC at their bank (issuing bank). The issuing bank sends the LC to the seller’s bank (advising bank, often acting as the confirming bank). The seller ships, prepares documents, and presents to their bank. If documents comply with LC terms, the bank pays.

Three key features:

Irrevocable. Once issued, the LC cannot be amended or cancelled without all parties’ consent. This is what gives the seller assurance.

Documentary. The LC pays against documents, not against actual goods. Banks deal with paper. The documents typically required: commercial invoice, packing list, bill of lading, certificate of origin, certificate of analysis, inspection certificate. Some LCs require additional documents (Phytosanitary, fumigation, halal, etc.).

UCP 600 governance. International Chamber of Commerce’s Uniform Customs and Practice for Documentary Credits, 2007 revision. Defines how LCs operate worldwide. Most commercial LCs are issued subject to UCP 600.

Confirmed vs unconfirmed

An unconfirmed LC is paid by the issuing bank only. The seller bears the issuing bank’s credit risk and the country risk of the issuing bank’s jurisdiction.

A confirmed LC adds a second bank’s guarantee. The confirming bank (usually in the seller’s country or a major financial centre) commits to pay if the issuing bank does not. This is what sellers in emerging-market trade ask for when the issuing bank is in a higher-risk jurisdiction.

Confirmation cost is typically 0.5-2% per annum of the LC value, depending on the issuing bank’s jurisdiction and rating.

Sight vs deferred

A sight LC pays the seller on presentation of compliant documents. The buyer pays immediately. Cash flow: tight.

A deferred LC (also called usance LC) pays the seller a specified period after document presentation — typically 30, 60, 90, or 180 days. Common in commodity trade because it gives the buyer working capital flexibility. The discount cost (the buyer effectively borrowing from the bank) is built into the price.

A typical commodity transaction structure: 90-day deferred LC at sight, with the seller able to discount the LC at their bank for immediate funds. The discount cost (LIBOR/SOFR + margin) is paid by the seller.

SBLC: performance, not payment

A Standby Letter of Credit is structurally similar to an LC but functions as a guarantee, not a primary payment instrument. The SBLC sits behind a contract. The seller draws on the SBLC only if the buyer defaults on payment under that contract.

Typical use cases:

- Long-term supply contracts. A 12-month or 24-month offtake contract. The seller wants assurance the buyer will pay. The SBLC, issued for, say, 110% of one month’s expected purchase value, sits behind the contract.

- Performance backing for the seller. Some contracts require the seller to post an SBLC to guarantee delivery. Less common but used.

SBLC opening cost: typically 0.5-1.5% per annum of the SBLC value. Funded SBLCs (where the issuing bank requires cash collateral) are cheaper; unfunded SBLCs (issued against the applicant’s credit facility) are more expensive.

TT: when wire transfer is the right answer

Telegraphic Transfer (TT) is direct bank-to-bank wire. No conditions, no documentary trigger — the buyer simply instructs their bank to send money to the seller. SWIFT MT103 is the typical message format.

TT works when:

- The counterparty is established and trusted. Years of dealing, established trust, no defaults.

- The transaction value is moderate. TT is fine for $50,000-500,000. For multi-million-dollar cargoes, most buyers prefer LC structure.

- Speed matters. A TT lands in the seller’s account within hours. An LC opens in days.

Typical TT structure in commodity trading:

- 30% TT against pro-forma invoice (PI). Down payment before shipment.

- 70% TT against documents. Balance against bills of lading and inspection certificates.

This structure is common in marine fuel bunker contracts (which are typically lower-value and counterparty-known), in fly ash trade (where ongoing relationships are established), and in small-volume metal concentrate trade.

The risk for the seller in a TT structure is that the buyer may not pay the balance after taking the documents. Sophisticated sellers retain title until full payment is received.

Documentary collection: D/P and D/A

Documentary collection is a less-used but useful instrument:

- D/P (Documents against Payment). Buyer’s bank releases documents to the buyer only after the buyer pays.

- D/A (Documents against Acceptance). Buyer’s bank releases documents to the buyer after the buyer accepts a bill of exchange — promising to pay at a specified later date.

Documentary collection is cheaper than LC (no bank guarantee, just a document-handling service) but riskier for the seller. If the buyer refuses to pay or accept, the seller has goods on the wharf at the destination port with no buyer.

Use cases are situational: established counterparties in jurisdictions where LC issuance is expensive or slow; low-value cargoes where LC fees would be disproportionate.

Escrow: when neither party trusts the other

Escrow is uncommon in commodity trade but appears in specific scenarios:

- New counterparty with no track record

- Distressed asset purchase

- Contested transaction (e.g., quality dispute under arbitration)

A third party (typically a law firm or specialised escrow service) holds funds. Funds release on specified conditions. Most commodity transactions can be structured without escrow using LC, but for specific high-uncertainty deals it is the right tool.

Bank fees: what to budget

Approximate fee ranges (vary by bank, jurisdiction, transaction size):

Service | Typical fee |

LC issuance | 0.1-0.5% per quarter of LC value |

LC confirmation | 0.5-2% per annum of LC value |

LC discrepancy fee | $75-200 per discrepancy |

LC amendment | $100-300 per amendment |

SBLC issuance | 0.5-1.5% per annum |

TT (outgoing) | $20-100 per transfer |

Discounting (deferred LC) | LIBOR/SOFR + 0.5-2% per annum |

The discrepancy fee deserves attention. Banks examine LC documents strictly. A typo, a date inconsistency, a misspelling — any discrepancy triggers a fee and may delay payment. Sophisticated commodity traders maintain LC documentation checklists to minimise discrepancies.

Document set: what must travel with the cargo

A standard commodity LC document set:

- Commercial invoice — describes goods, price, quantity

- Packing list — itemises individual units

- Bill of lading (B/L) — title document; states shipper, consignee, goods, vessel, ports

- Certificate of origin — issued by chamber of commerce; states country of origin

- Certificate of analysis (COA) — chemistry and quality verification

- Inspection certificate — SGS, Alex Stewart, Intertek, or equivalent

- Insurance certificate — for CIF terms only; states marine insurance cover

Some LCs require additional documents:

- Phytosanitary certificate (organic materials, some industrial minerals)

- Fumigation certificate (containerised cargo, agricultural products)

- Test certificate (specific to commodity, e.g., assay certificate for metals)

- Beneficiary statement (specific declarations like “non-Russian origin”)

The document set must match the LC exactly. A buyer who specifies “SGS inspection certificate” in the LC and accepts an Intertek certificate has accepted a discrepancy.

Commodity-by-commodity guidance

Au Club’s working approach to payment structure by commodity:

Marine fuel (VLSFO, HSFO). Typically TT — 30/70 or 50/50 against pre-shipment documents and bunker delivery note. Established counterparty preferred. LC used for first-time customers or for large cargoes.

Copper cathode. LC standard. Confirmed irrevocable, sight or 90-day deferred. Documents: COA, COO, LME warrant, BL, inspection certificate, non-Russian-origin statement.

Antimony. LC standard. The high unit value and origin sensitivity make TT unattractive. 90-day deferred LC is common.

Tin concentrate. LC for international refinery buyers. Deferred LC (60-90 days) is the standard.

Tungsten concentrate. LC standard. Documents include WO₃ assay certificate, COO, BL.

Tungsten scrap. LC for large lots; TT for smaller lots with established counterparties.

Molybdenum oxide. LC standard. Deferred LC (60-90 days) common.

Fly ash. TT or LC. Multi-year contracts often use LC structure to formalise the relationship. Spot smaller deliveries often use TT.

How to open an LC: a working sequence

For a buyer opening an LC against a confirmed Au Club purchase:

- Confirm the contract terms with Au Club. Volume, specification, delivery terms (FOB/CFR/CIF), payment terms.

- Approach your bank’s trade-finance desk. Provide the contract or PI.

- Complete the LC application form. Your bank will draft the LC for review.

- Review LC terms with Au Club. Au Club confirms the document requirements and any specific clauses.

- Your bank issues the LC. Sent via SWIFT to Au Club’s bank.

- Au Club’s bank confirms receipt. Au Club receives the LC text.

- Au Club ships and prepares documents. Documents presented to bank.

- Bank pays Au Club (sight LC) or accepts and pays at maturity (deferred LC).

The cycle from application to LC issuance typically takes 3-10 business days depending on the bank.

Au Club’s preferred payment structures

Au Club accepts LC and TT. Our preferred structures by typical commodity:

Commodity | Preferred structure |

Marine fuel | TT 30/70 or established credit terms |

Antimony, tungsten, moly | Confirmed irrevocable LC, 60-90 day deferred |

Copper cathode | Confirmed irrevocable LC, sight or 90-day |

Tin concentrate | LC, 60-90 day deferred |

Fly ash | TT or LC depending on volume |

For first-time buyers, we typically require confirmed LC from a top-tier bank. After successful transactions and established relationship, TT structures are available for smaller-value or established categories.

FAQs

What is the difference between LC and SBLC?

LC is the primary payment instrument — the bank pays when documents are presented. SBLC is a guarantee — the bank pays only if the buyer defaults under the underlying contract.

Is a TT safe for commodity payments?

Safer for established counterparties and smaller transactions. For new counterparties or high-value transactions, LC is the more protective structure for both parties.

How long does it take to open an LC?

Typically 3-10 business days from application to issuance, depending on the bank and the complexity of the LC text.

Why do some LCs cost more than others?

LC pricing reflects the issuing bank’s risk on the buyer (creditworthiness), the country risk of the buyer’s jurisdiction, and the confirmation cost if the LC is confirmed. Emerging-market buyer LCs cost more than OECD-buyer LCs.

About Au Club

Au Club accepts LC and TT for commodity transactions. Confirmed irrevocable LCs from top-tier banks are our standard payment instrument for high-value metals and minerals. Established TT relationships are available for marine fuel and certain mineral categories. Contact our trading desk to discuss appropriate payment structure for your purchase.