Molybdenum 2026 Outlook: Why the Stainless Steel Cycle Looks Different This Time

Molybdenum in the US reached $50,265 per metric ton in June 2025. Chinese 45% molybdenum concentrate hit a record 4,600 CNY per ton-unit in early September 2025. Ferromolybdenum peaked at 293,000 CNY per ton. This cyc…

Molybdenum in the US reached $50,265 per metric ton in June 2025. Chinese 45% molybdenum concentrate hit a record 4,600 CNY per ton-unit in early September 2025. Ferromolybdenum peaked at 293,000 CNY per ton. This cycle has familiar surface drivers — stainless steel demand, supply tightness — but three structural features make it different from any moly cycle of the past twenty years. This article walks through what is unusual, models 2026 base, bull, and bear scenarios, and explains how procurement teams should write next year’s contracts.

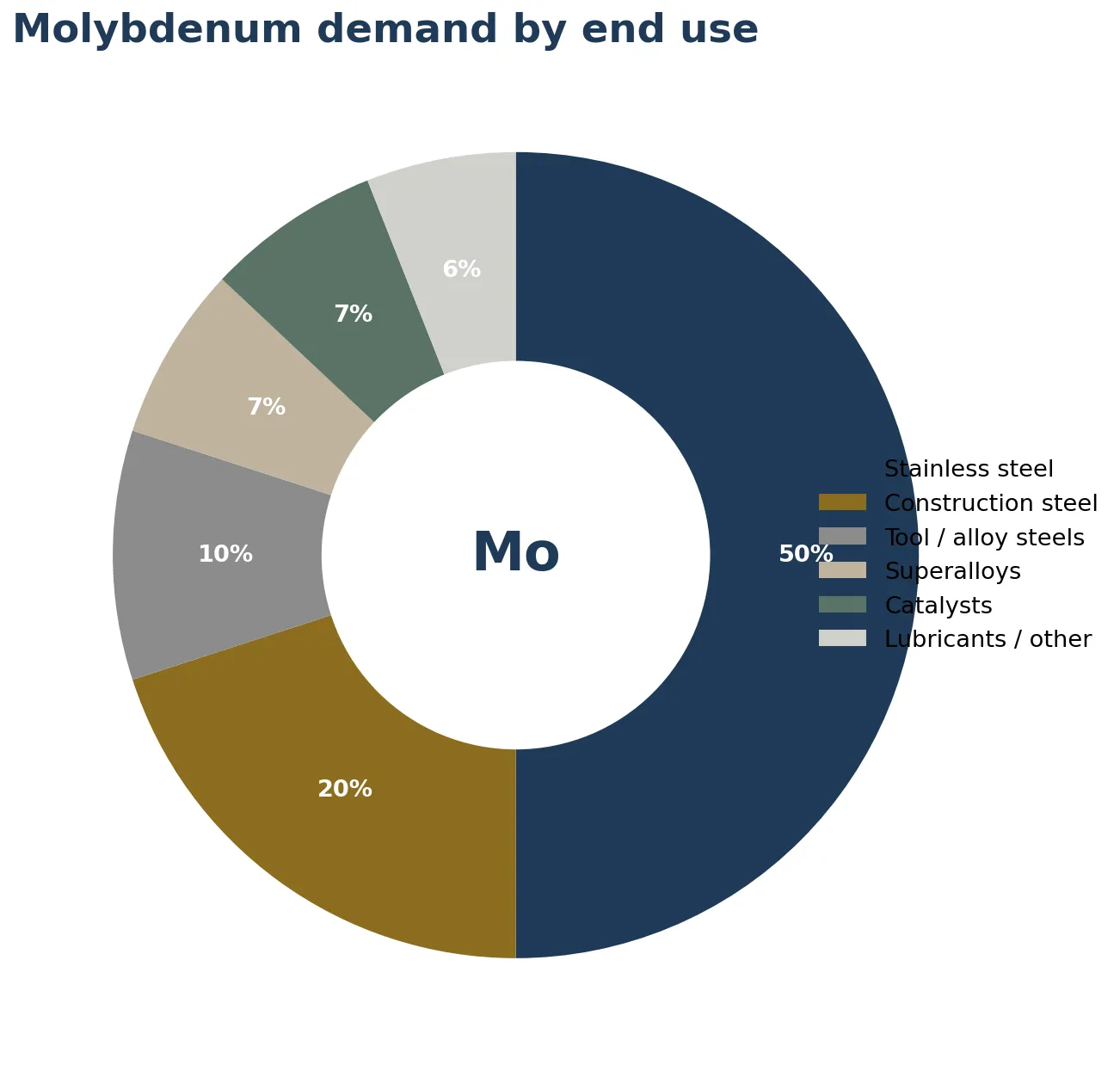

Where moly is consumed

Molybdenum has narrow but high-value end uses:

End use | Share of demand |

Stainless steel (especially 316 grades, duplex) | ~50% |

Construction / structural steel (HSLA grades) | ~20% |

Tool and alloy steels | ~10% |

Superalloys (turbines, aerospace) | ~7% |

Catalysts (petroleum refining, chemicals) | ~7% |

Lubricants and other | ~6% |

Stainless steel is the dominant end use. Moly improves corrosion resistance — 316 stainless contains 2-3% moly and is the standard for marine, food-processing, pharmaceutical, and chemical-process equipment. Duplex stainless contains higher moly content and is used for aggressive corrosion environments (offshore oil and gas, desalination, pulp and paper).

The other notable user is the petroleum refining industry. Moly-based catalysts are used in hydrodesulphurisation (removing sulphur from fuels) and hydrocracking. Refinery catalyst demand correlates with global refinery capacity.

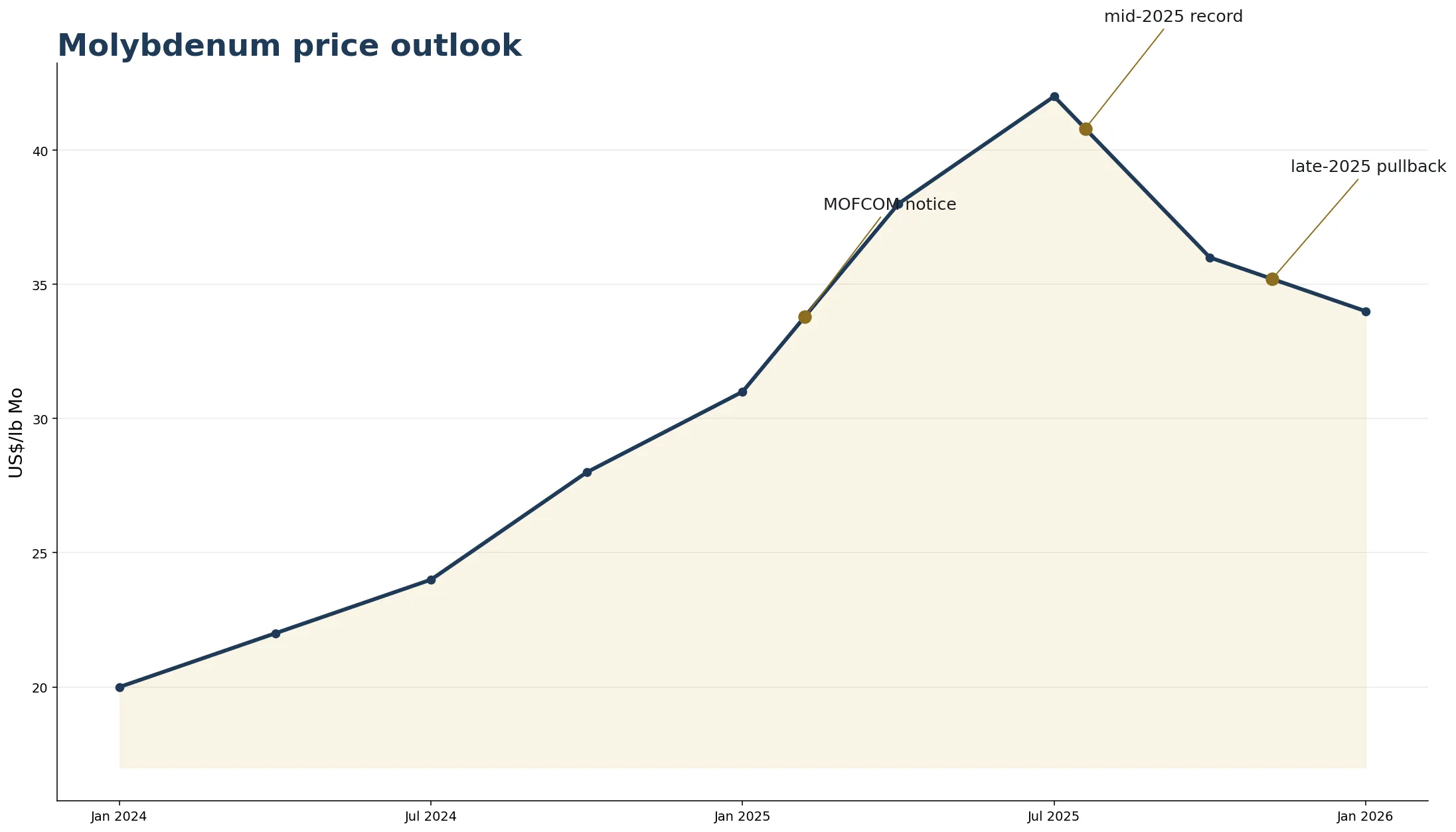

Recent price history

Mid-2024 to early 2026 has been a sustained uptrend:

Period | US moly price ($/MT) | Driver |

Q2 2024 | $32,000-35,000 | Steady stainless demand |

Q4 2024 | $38,000-42,000 | China export-control announcement (Feb 4, 2025) priced in early |

Q2 2025 | $48,000-52,000 | Demand acceleration + supply tightening |

Q3 2025 | $51,000-55,000 | Peak; Chinese concentrate record |

Q4 2025 | $48,000-52,000 | Modest pullback |

Q1 2026 | $46,000-52,000 (working range) | Stable elevated |

Chinese 45% moly concentrate at 4,600 CNY/MTU and ferromoly at 293,000 CNY/ton in September 2025 represent multi-year highs. Western and Chinese prices have moved in close correlation, with the Chinese export-control regime keeping a wedge open between the two.

What is structurally different about this cycle

Three features set the 2024-2026 moly cycle apart from prior cycles:

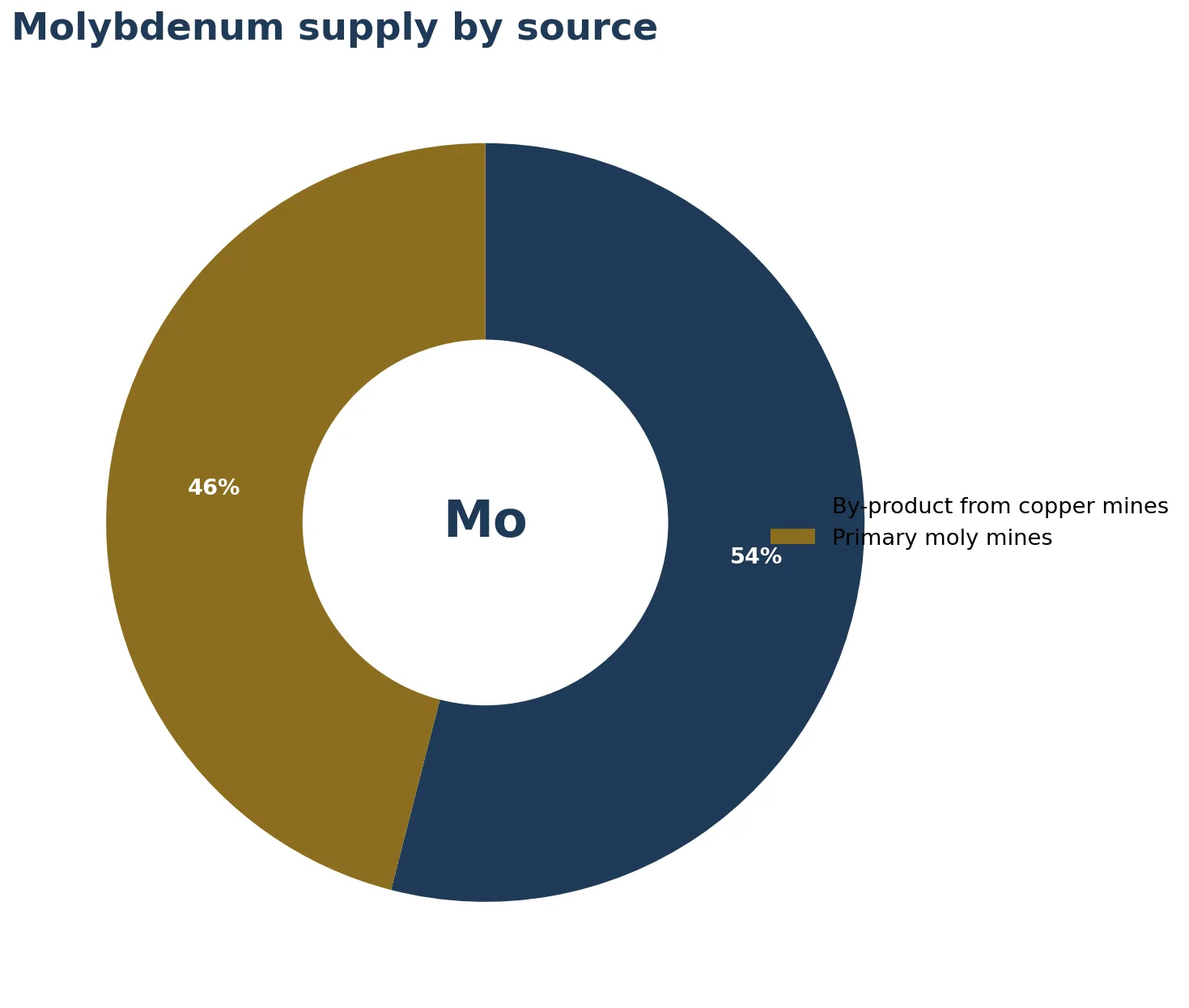

1. Half of the world’s moly is a by-product of copper

Approximately 50-55% of global moly is mined as a by-product of porphyry copper deposits. Codelco’s Chuquicamata, Freeport’s Grasberg and Cerro Verde, Antofagasta’s Centinela and Los Pelambres, Southern Copper’s Buenavista and Toquepala — these mines all produce significant moly as a co-product of copper.

This is structurally important. By-product moly supply is governed by copper economics. When copper prices are strong (as they have been in 2025), porphyry copper miners produce more — which means more moly. When copper prices are weak, porphyry production slows and moly supply tightens.

In normal cycles, moly demand and supply respond to moly economics. In this cycle, copper economics are pulling moly supply with them in unexpected ways. The 2025 copper price rise should have produced more moly. It did, but not as much as expected — because Chinese smelter pressure on copper concentrate kept some porphyry operators in cash-flow conservation mode.

2. Captive supply concentration is unusually tight

Of the non-by-product moly supply, a meaningful share is captive. Climax Molybdenum (Freeport subsidiary) operates the Henderson and Climax mines in Colorado, producing primary moly. China’s primary moly producers concentrate production for domestic use. The freely tradable global moly market is smaller than the production figures suggest.

When buyers like ATI, Outokumpu, Aperam, and Acerinox look for incremental supply, they compete for a relatively shallow tradable pool. That intensifies the price reaction to incremental demand.

3. The China export-control regime adds a wedge

The MOFCOM 4 February 2025 export-control notice placed moly on the dual-use items list along with tungsten, tellurium, bismuth, and indium. Chinese moly exports have continued under the licence regime — moly is less politically charged than antimony — but the licence-application friction has slowed cross-border movement.

The practical effect: a Chinese-Western price wedge has emerged. Western buyers pay a premium for non-Chinese moly. Chinese buyers (steel mills, chemical plants) source primarily from domestic supply. The arbitrage that would normally close this wedge has been reduced by licensing friction.

Demand-side: why stainless steel is structural this cycle

Stainless steel demand has been strong, and the drivers look durable:

Grid-scale electrification. Electric transmission infrastructure (high-voltage AC and DC transmission), substation equipment, and power-generation hardware use stainless steel extensively. The global electrification programme is producing sustained demand.

Hydrogen and chemical processing. Green hydrogen electrolysers, alkaline electrolysis equipment, and adjacent chemical processing infrastructure use high-grade stainless. Multi-billion-dollar electrolyser fleets are being built across Europe, the US, India, and the Middle East (including in Saudi Arabia and the UAE).

Aerospace. Both commercial aviation (recovering passenger traffic) and defence aerospace (escalating military procurement globally) drive demand for moly-bearing superalloys.

Desalination. Gulf state desalination capacity continues to expand. Reverse osmosis and multi-stage flash plants use duplex and super-duplex stainless extensively.

Lithium and battery chemicals. Lithium hydroxide processing, sulphate plants, and ammonia-based ammonia-water-electrolyte systems use moly-bearing alloys. New lithium chemicals capacity in Australia, Chile, and Argentina is driving demand.

The unusual feature: most of these demand sources are project-driven and long-cycle. They build out over years, not months. Stainless mills supplying these projects have multi-year order books. Moly demand from these projects is more visible than ordinary stainless demand.

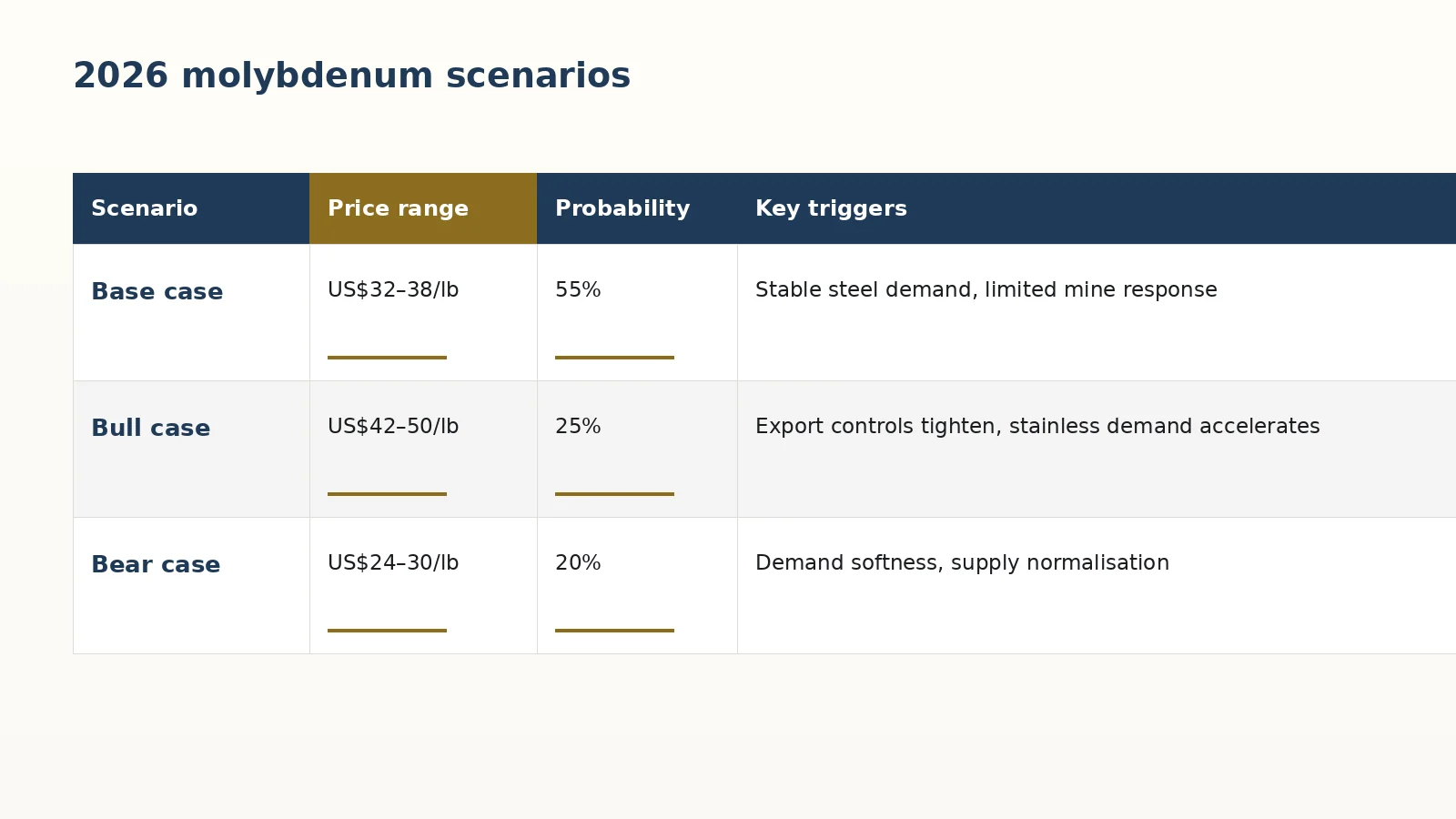

2026 scenarios

Au Club’s working scenario framework for 2026:

Base case (60% probability)

- Price range. US moly $42,000-52,000/MT. European moly oxide $20-25/lb Mo.

- Drivers. Stainless steel demand continues at strong levels. China export licences flow at moderate pace. By-product copper supply ramps modestly. No major mine disruption.

- Implications for buyers. Lock 12-month supply at current pricing. Multi-year contracts at modest premium are available.

Bull case for prices (25% probability)

- Price range. US moly $55,000-65,000/MT.

- Drivers. Significant additional supply restrictions from China (full export ban scenario). Major mine disruption at a key porphyry operation. Acceleration of hydrogen project demand.

- Implications for buyers. Forward purchases at elevated levels become necessary. Stockpile becomes economic to hold.

Bear case for prices (15% probability)

- Price range. US moly $32,000-42,000/MT.

- Drivers. Chinese export-control regime relaxed in a broader US-China trade deal. Stainless steel demand falls in a global recession. New mine supply ramps faster than expected.

- Implications for buyers. Defer forward purchases; buy spot.

How to write a 2026 moly contract

Three contract elements that matter:

1. Price formula. Most international moly oxide contracts price as a discount or premium to a published benchmark — typically Platts moly oxide or Fastmarkets moly oxide assessment. Avoid fixed-price for 12-month or longer contracts; the price volatility is too high. Use a published benchmark + premium/discount structure.

2. Origin clause. Specify whether the buyer requires non-Chinese material. The current pricing wedge between Chinese and non-Chinese moly oxide is meaningful. Buyers with US, EU, or defence-adjacent end markets typically specify non-Chinese origin.

3. Volume flexibility. Build in seasonal or monthly volume flexibility (±10% typical). Demand from steel-mill buyers and refinery catalyst buyers is not perfectly stable; the contract should accommodate.

Au Club’s offer

Au Club supplies molybdenum oxide (MoO₃, 63% Mo minimum) with 300 MT/month availability. Non-Chinese origin available for buyers with that requirement. FOB UAE, SGS inspection. LC and TT accepted.

The Au Club desk maintains active relationships with primary moly producers in Chile, Peru, Mexico, the US, and a number of by-product copper operators. We can structure spot, monthly offtake, and multi-year supply for buyers with appropriate requirements.

Au Club’s read for 2026

Three working positions:

- Moly does not return to early-2024 prices in 2026. The structural drivers — stainless demand, China export friction, supply concentration — keep prices elevated. The base case range is $42,000-52,000/MT.

- The Chinese-Western wedge persists. Non-Chinese moly continues to trade at a meaningful premium. Buyers with non-Chinese specifications should plan around this.

- 2027-2028 brings potential supply easing. New by-product moly from ramping copper projects (Kamoa-Kakula expansions, Oyu Tolgoi underground full ramp, Indonesian copper smelter build-out) adds supply. Whether that arrives in time for 2027 depends on copper project execution.

For procurement teams: lock 2026 supply at current pricing. Engage now for 2027-2028 forward arrangements. Do not wait for Chinese policy clarity that may not arrive.

FAQs

What is moly oxide?

Molybdenum trioxide (MoO₃) is the primary tradable form of molybdenum. Typical commercial grade is 63% Mo minimum (corresponding to approximately 95% MoO₃ purity). Sold in 250-kg drums or 1-MT super-sacks.

What is the current moly price?

US moly prices in early 2026 are trading in the $46,000-52,000/MT range. For real-time pricing, contact our trading desk or check Platts and Fastmarkets assessments.

Where does Au Club source molybdenum oxide?

Multiple producers, with the option of confirmed non-Chinese origin for buyers who require it. Primary sources in the Americas (Chile, Peru, US, Mexico) and selected by-product operations.

Will the moly price come back down?

Au Club’s base case for 2026 is sustained elevated pricing ($42,000-52,000/MT US). A meaningful decline requires either a US-China trade resolution or a stainless steel demand contraction — neither is signalled for 2026.

About Au Club

Au Club supplies molybdenum oxide (MoO₃, 63% Mo minimum) with 300 MT/month availability. FOB UAE, SGS inspection. LC and TT accepted. Contact our trading desk to discuss 2026 and 2027 supply.