LNG, Methanol, Biofuel: The 2027 Marine Fuel Transition and What It Means for Fujairah

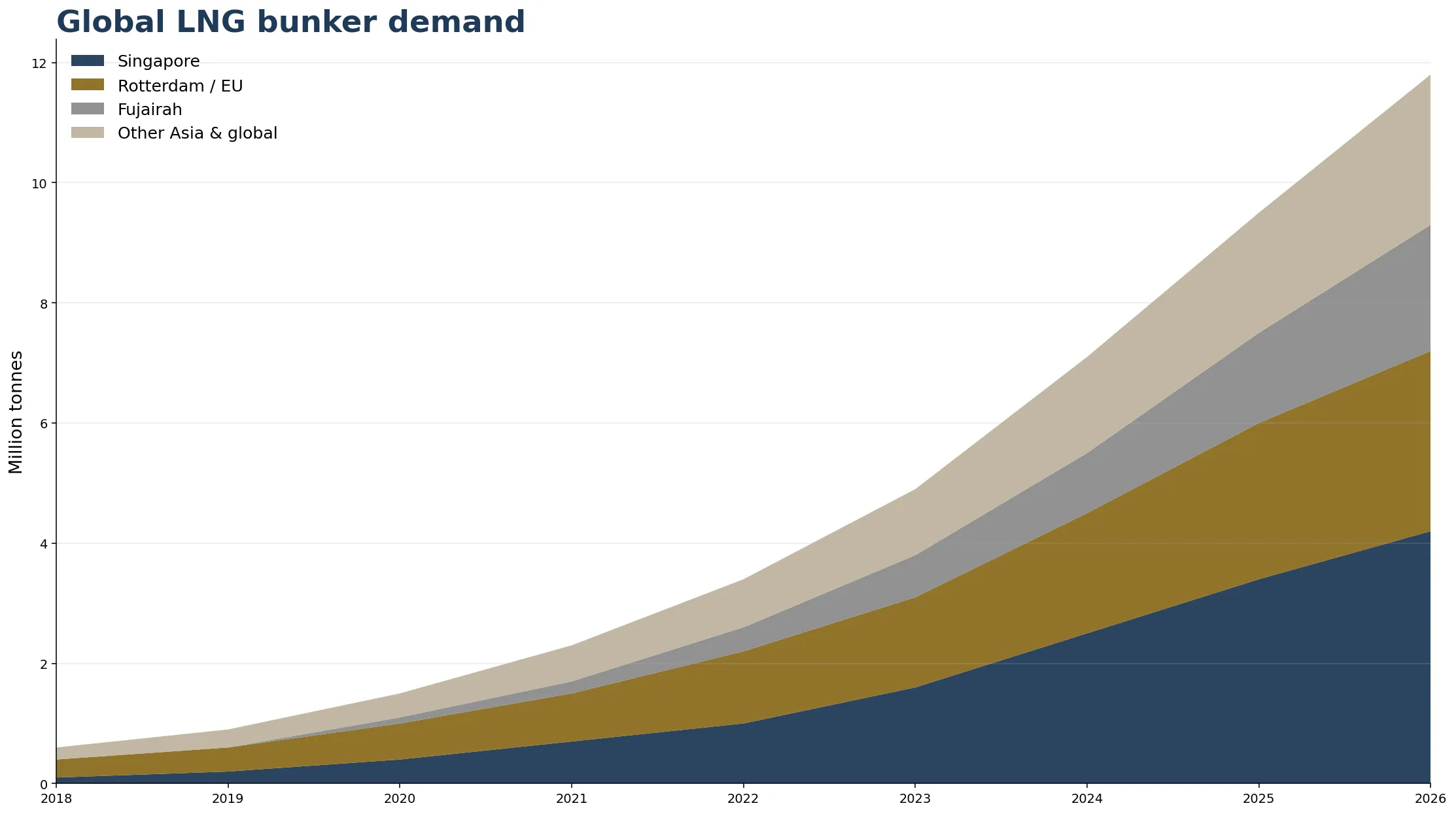

Singapore moved 463,948 metric tons of LNG bunker fuel in 2024, up over four-fold from the year before. Global LNG bunker demand reached approximately 4 million MT in 2025, up 54% year-on-year. ADNOC and TotalEnergies…

Singapore moved 463,948 metric tons of LNG bunker fuel in 2024, up over four-fold from the year before. Global LNG bunker demand reached approximately 4 million MT in 2025, up 54% year-on-year. ADNOC and TotalEnergies added 18,000 m³ of floating LNG storage to Fujairah in early 2026, positioning the Gulf to intercept Asia-Europe trade lanes. On 1 March 2027 the IMO Net-Zero Framework enters force, applying carbon prices of up to $380 per ton CO₂e to vessels that exceed the GHG intensity target. The next three years are the bunker market’s transition window. This article maps where each alternative fuel actually stands, what Fujairah’s role becomes, and how operators should be planning bunker strategy for 2027 and beyond.

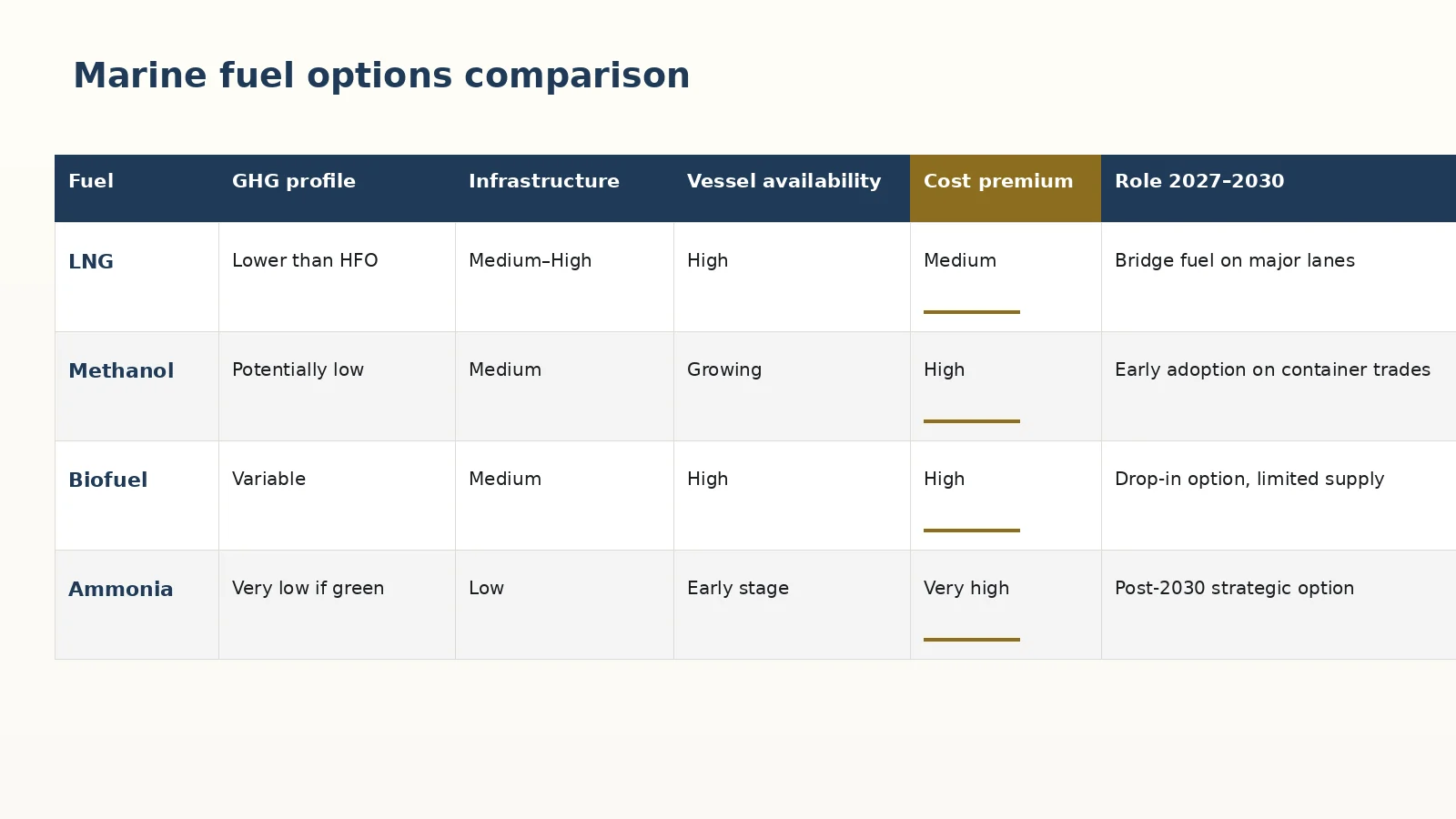

The four alternatives, and where each stands

Operators have four credible non-conventional fuel paths. Each is at a different point on the readiness curve:

Fuel | Readiness | Infrastructure status | GHG intensity vs HFO | Commercial vessels in fleet |

LNG | Commercial scale | Singapore, Rotterdam, Zeebrugge, Yokohama, Fujairah (growing) | -20% to -25% | 1,500+ |

Methanol | Early commercial | Singapore, Rotterdam, Antwerp; limited Asian and Gulf coverage | -10% to -90% (depending on production) | 200+ in service or on order |

Biofuel (drop-in) | Operationally available | Singapore (B24/B30), Rotterdam, Algeciras, Houston | -30% to -85% (depending on blend and feedstock) | Most modern vessels can burn B24/B30 |

Ammonia | Pilot / first vessels | Limited; under development | -75% to -90% (blue or green) | 5-10 in service, large order book 2027+ |

The numbers shift quickly. LNG’s lead is substantial — 1,500+ vessels in service or on order — but methanol orders accelerated through 2024-2025 as Maersk, CMA CGM, and Hapag-Lloyd commissioned dual-fuel methanol new-builds. Biofuel is the easiest transition path for existing vessels because it can blend with VLSFO and HSFO without machinery modification.

LNG: the dominant alternative for the next 5-10 years

LNG bunker demand grew from approximately 2.6 million MT in 2024 to about 4 million MT in 2025 — a 54% increase. Singapore’s growth has been the most striking: from 111,000 MT in 2023 to 463,948 MT in 2024, with 401,200 MT in the first three quarters of 2025 alone (heading for a similar full-year volume).

The supply chain has built out:

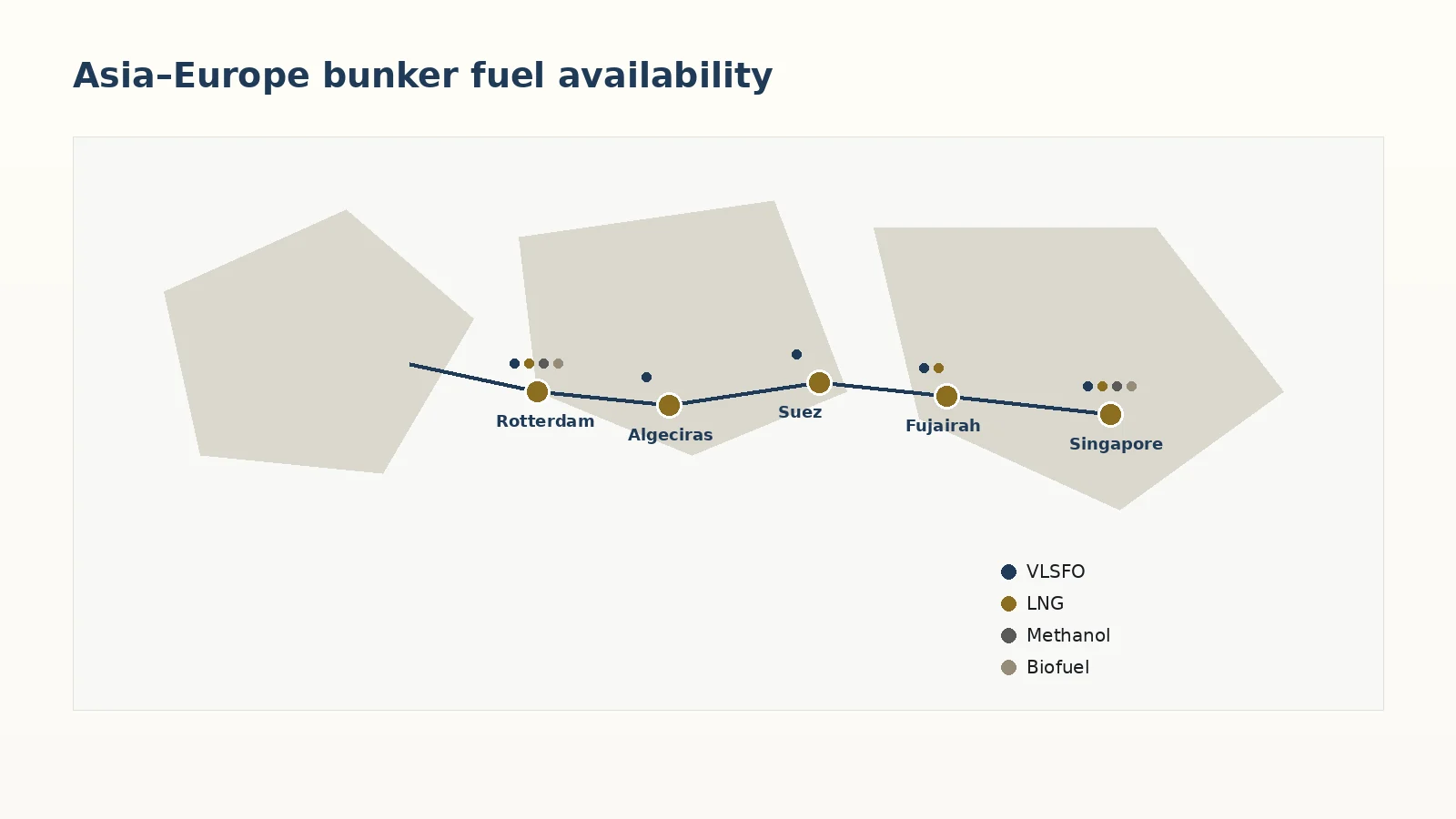

- Singapore. The world’s largest bunker hub. Multiple LNG bunker vessels operate. December 2024 MPA Expression of Interest seeking scalable solutions for sea-based LNG reloading. Singapore is positioned to remain the global LNG bunker leader.

- Rotterdam. Established LNG bunker capacity. Northern European hub for the Asia-Europe lane.

- Yokohama and northern Asian ports. Growing capacity. Japanese and South Korean ports moving to commercial LNG bunkering.

- Zeebrugge. Significant LNG terminal capacity. Belgian bunker market growing.

- Fujairah. ADNOC-TotalEnergies floating storage (18,000 m³) added in early 2026. Positioning to serve eastbound and westbound Asia-Europe routings.

A 14,000-TEU container vessel running on LNG produces approximately 20-25% less CO₂ than the same vessel on VLSFO on a tank-to-wake basis. On a well-to-wake basis (accounting for upstream methane slip and LNG production emissions), the saving is smaller — typically 15-20% — but still meaningful under the MEPC 83 framework.

Methanol: the alternative that catches up fast

Methanol production has scaled and the fuel can be made from multiple feedstocks. Three categories matter:

- Grey methanol. Produced from natural gas. Cheapest, but minimal GHG benefit over conventional bunker fuel (the carbon savings depend on production process).

- Blue methanol. Produced from natural gas with carbon capture. Meaningful GHG savings (40-70%) but limited commercial production.

- E-methanol (green). Produced from CO₂ + renewable hydrogen. Largest GHG savings (90%+) but small commercial volume and high cost.

Maersk has been the most aggressive methanol adopter, with 25+ dual-fuel methanol vessels in service or on order. CMA CGM has signed up. Hapag-Lloyd and several others have followed. The maritime methanol fleet is small today but growing rapidly.

Where methanol can be bunkered:

- Singapore. Commercial methanol bunkering operational; multi-supplier.

- Rotterdam. Established methanol bunker capacity.

- Antwerp. Growing capacity.

- Houston and US Gulf. Limited but expanding.

- Asia and Middle East. Limited; growing.

The MEPC 83 framework heavily favours methanol because of its well-to-wake GHG intensity. A Maersk-class methanol vessel running on green methanol generates significant Surplus Units that can be sold or transferred — making the economics work even at a higher fuel cost.

Biofuel: the path for the existing fleet

Biofuel blends (HFO + biodiesel, or VLSFO + biodiesel) are the simplest transition. Most modern vessels can burn B24 (24% biofuel) or B30 (30% biofuel) without major machinery modification.

B24 / B30 is operational at Singapore and Rotterdam. Singapore conducted the first commercial B100 (100% biofuel) bunker trial in 2022 and has scaled biofuel bunker sales meaningfully through 2024-2025. ISO 8217:2024 includes specifications for biofuel blends.

The carbon saving depends on feedstock and blend:

- B24 with used cooking oil (UCO) feedstock: approximately 20-25% well-to-wake GHG saving

- B30 with UCO: approximately 25-30% saving

- B100 with UCO: 80-85% saving

Sustainable biofuel feedstocks are constrained. UCO supply is limited. Agricultural feedstocks (palm oil, soy) face sustainability scrutiny. The IMO MEPC 83 framework recognises only sustainable biofuels — the precise criteria are being refined.

For existing vessels facing the 1 March 2027 framework, biofuel blends are the most cost-effective compliance pathway. Operators can buy a biofuel blend at a premium and earn Surplus Units or avoid Remedial Units.

Ammonia: the longer-term path

Ammonia (NH₃) has zero direct CO₂ emissions on combustion. Made from renewable hydrogen plus nitrogen, it offers a near-complete decarbonisation pathway.

The 2025-2026 status:

- A handful of ammonia-fuelled vessels are in service or commissioning

- The order book for ammonia dual-fuel vessels grew through 2024-2025

- Production capacity at scale (green ammonia from renewable hydrogen) is starting to come online in Saudi Arabia (NEOM Green Hydrogen Mega-Project), Oman, Australia, and Egypt

- Bunker infrastructure is at pilot scale only

Practical commercial ammonia bunkering at scale is a 2028-2030 story. Significant safety, infrastructure, and crew-training challenges remain. For 2026-2027 planning, ammonia is a watching brief rather than an active option.

What Fujairah’s role becomes

Fujairah’s strategic position changes meaningfully over the next three years. The port has three structural advantages:

Geographical positioning. East of the Strait of Hormuz, outside the Persian Gulf, on the natural shipping lane between Asia and Europe / Africa / Africa-routed bunkering.

Storage depth. Vopak, Concord, ADNOC, ENOC, and others operate substantial liquid storage. The ADNOC-TotalEnergies floating LNG capacity (added early 2026) brings LNG into the bunker portfolio at scale.

Supplier competition. 35+ physical bunker suppliers create the tightest bid-stack in the Middle East region.

Fujairah’s working role in the transition:

Fuel | Fujairah role 2027 onwards |

VLSFO / HSFO | Continued dominant supply hub for conventional bunker |

LNG | Emerging hub via ADNOC-TotalEnergies; could absorb Asia-Europe LNG bunker demand |

Biofuel blends | B24 / B30 entering the bunker portfolio through 2027-2028 |

Methanol | Limited near-term; potentially developing 2028-2030 |

Ammonia | Future consideration; NEOM and Oman green ammonia projects regional |

The Gulf’s natural advantages for the alternative-fuel transition are real. Abundant renewable energy (solar in Saudi, UAE, Oman) supports green ammonia production. Established LNG infrastructure (Qatar, UAE) supports LNG bunker. The shipping lane between Asia and Europe runs past the door.

What an operator should do this quarter

Practical actions for an operator preparing for the 1 March 2027 framework:

- Quantify current fleet exposure. Calculate annual bunker consumption, average GHG intensity, and projected MEPC 83 Remedial Unit cost at 2027 prices.

- Identify the lowest-cost compliance pathway. For most operators of existing vessels, biofuel blends are the lowest-cost partial-compliance path. For new-builds, LNG or methanol dual-fuel.

- Open relationships with multiple bunker suppliers. Auto-pilot single-supplier relationships need to expand. Au Club and other multi-fuel suppliers provide flexibility across grades.

- Update charter parties. 2026 fixtures should include explicit clauses for bunker grade flexibility, RU cost allocation, and Surplus Unit ownership.

- Plan vessel-level monitoring. MEPC 83 will require well-to-wake intensity measurement and reporting. Onboard fuel monitoring and IT integration with shore compliance teams is becoming standard.

Au Club’s read for 2027 and beyond

Three working positions:

- VLSFO remains the largest single bunker grade through 2027. Total alternative-fuel bunker demand will likely exceed 6 million MT globally in 2027 but VLSFO will still dominate at 250+ million MT annually.

- Fujairah grows materially as an LNG bunker hub. The ADNOC-TotalEnergies floating storage and the Gulf’s natural energy advantages make Fujairah a credible alternative to Singapore for LNG bunkering on Asia-Europe routings.

- Biofuel blends become routine. By 2028, B24 / B30 blends will be available at most major bunker hubs as standard offerings. Operators not already in conversation with biofuel suppliers are behind the curve.

For procurement teams: 2026 is the year to qualify alternative-fuel suppliers, restructure bunker contracts, and validate vessel-level compliance pathways. 2027 is the year of actual implementation. Operators who wait will pay disproportionately for late-stage compliance.

FAQs

When does the IMO Net-Zero Framework enter force?

1 March 2027. The framework was approved at MEPC 83 (April 2025) and adopted at the extraordinary MEPC session in October 2025.

Should I order a new-build with LNG or methanol dual-fuel?

For most operator profiles in 2026, both options are viable. LNG has stronger near-term infrastructure; methanol has stronger long-term GHG positioning. The decision depends on trade lane (LNG strong for Asia-Europe; methanol strong for transatlantic), refuelling network expectations, and operator strategy on Surplus Unit generation.

Can I burn biofuel in my existing vessel?

Most modern vessels (built post-2000 approximately) can burn B24 or B30 blends without machinery modification. Higher blends may require modification. Consult engine manufacturer documentation and class society.

Is Fujairah bunkering LNG?

Yes, since the early 2026 commissioning of ADNOC-TotalEnergies floating storage. LNG bunker volume is small today but growing. Fujairah is positioning to be a regional LNG bunker hub by 2027-2028.

About Au Club

Au Club supplies VLSFO (0.5% S) and HSFO (3.5% S) marine fuels at Jebel Ali, Port Khalifa, Fujairah, and Khor Fakkan. We work with customers on multi-year supply structures that anticipate MEPC 83 compliance and the alternative-fuel transition. Contact our bunker desk to discuss 2027-2030 strategy.