China Just Added Tungsten and Molybdenum to Its Export Control List. What Happens Next.

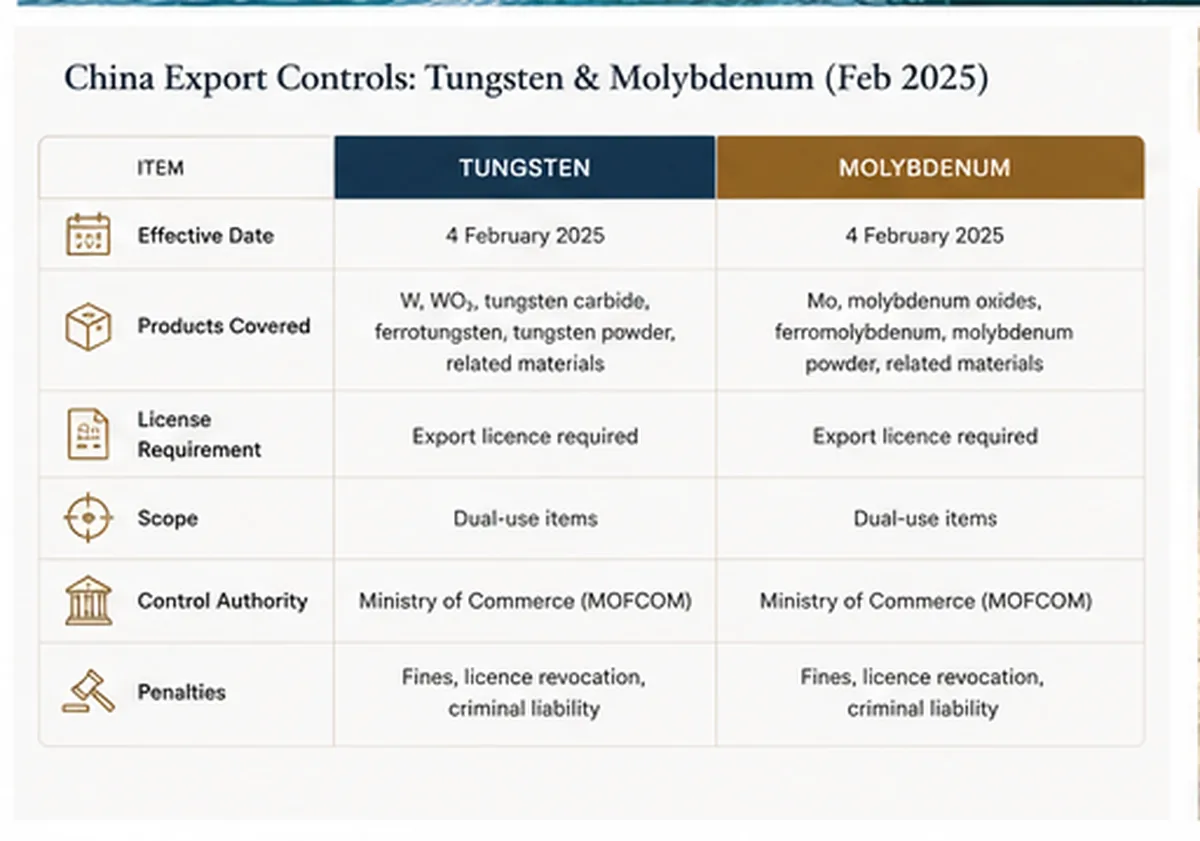

On 4 February 2025 MOFCOM placed tungsten, tellurium, bismuth, indium and molybdenum on China’s dual-use items export control list. This is the same mechanism that took antimony from $1,400 to $51,000 per metric ton i…

On 4 February 2025 MOFCOM placed tungsten, tellurium, bismuth, indium and molybdenum on China’s dual-use items export control list. This is the same mechanism that took antimony from $1,400 to $51,000 per metric ton in six months. China supplies roughly 80% of world tungsten and is a dominant molybdenum producer. The price reaction has not yet matched antimony’s, but the mechanism is identical, the precedent is fresh, and the structural picture for Western buyers of APT, ferro-tungsten, and molybdenum oxide is now materially different from what it was a week ago.

What the 4 February notice actually says

The MOFCOM announcement adds export licensing requirements for tungsten, tellurium, bismuth, molybdenum, and indium and their related items. As with the September 2024 antimony notice:

- Exporters must apply for individual licences for each shipment

- End-user and end-use disclosure is required

- Supporting documentation must accompany each application

- MOFCOM retains discretion over which licences are approved

- No country is named in the restriction, but the timing — five days after the US announced 10% tariffs on Chinese imports — is unambiguous

What the notice does not say is when licences will be approved, what criteria will apply, or whether dual-use civilian applications (cutting tools, stainless steel, lubricants) will be treated differently from defence-adjacent applications (armour-piercing rounds, missile guidance, superalloys).

The antimony precedent is informative. In the months after the September 2024 antimony licence regime took effect, Chinese exports collapsed by approximately 97%. Few licences have been granted publicly. Sources close to MOFCOM have described the approval rate as deliberate and quiet.

Why tungsten is the more strategic of the two

China accounts for approximately 80% of world tungsten mine production. The next largest producers are Vietnam (~5%), Russia (~3%), and a handful of smaller producers in Bolivia, Portugal, Spain, Rwanda, and Austria. The world’s commercially significant tungsten flow has gone through Chinese smelters for thirty years.

Tungsten is irreplaceable in specific applications. Its melting point (3,422°C) and density (19.3 g/cm³) make it the dominant material for:

- Cutting tools — tungsten carbide inserts for machining steel, aluminium, and composites

- Armour-piercing ammunition — kinetic energy penetrators (replacing depleted uranium in some military applications)

- Filaments and electrodes — though incandescent applications have declined, TIG welding electrodes and X-ray tube anodes still rely on tungsten

- Heavy alloys — radiation shielding, gyroscope rotors, counterweights

- Superalloys — turbine blades, where tungsten is alloyed with nickel and other refractory metals

The substitution path is poor. Cubic boron nitride substitutes for some cutting-tool applications but at higher cost. Synthetic diamond cuts certain materials better but cannot replace tungsten carbide across the board. There is no substitute at all for tungsten in heavy alloy and ammunition applications.

The price reaction so far

By early June 2025, European ammonium paratungstate (APT) prices were up over 40% from the start of the year. European ferro-tungsten rose 17.6%. The 4 February announcement was the catalyst; the actual licence approvals (or non-approvals) have driven the rolling repricing through Q1 and Q2.

Tungsten benchmark price moves, Jan–June 2025

Benchmark | Jan 2025 | June 2025 | Change |

European APT (USD/MTU WO₃) | $300 | $425+ | +40%+ |

European ferro-tungsten (USD/kg W) | $34 | $40 | +17.6% |

Chinese 65% concentrate (CNY/MTU) | 110,000 | 138,000 | +25% |

A material number of tungsten APT consumers — particularly mid-sized cutting tool manufacturers in Germany, Italy, the US, and Japan — have reported difficulty securing 2026 supply at any forward-priced contract.

Molybdenum: less concentrated than tungsten, but exposed to the same mechanism

Molybdenum is structurally different. Roughly half the world’s moly is mined as a primary product (in places like New Mexico, Chile, China). The other half is a by-product of copper porphyry mining at Codelco, Freeport, Antofagasta, and several other large copper producers. That diversification provides some structural cushion against any single producer.

But China is still the largest moly producer at approximately 40% of global supply. And Chinese moly oxide refining serves global steel mill markets. The MOFCOM licence regime applies to molybdenum and related items — including ferromolybdenum and moly oxide. If approvals slow, the impact lands on Western stainless steel mills, aerospace alloy producers, and lubricant additive manufacturers.

Through Q2 2025, US moly prices reached $50,265 per MT and Chinese 45% concentrate hit a record 4,600 CNY/ton-unit. The licence regime is one of several drivers (stainless steel demand from grid-scale infrastructure has been strong), but it is a meaningful share of the move.

Where non-Chinese tungsten and molybdenum lives

Au Club’s working view of non-Chinese supply for both metals:

Non-Chinese tungsten

Country | Producer / mine | Indicative output | Notes |

Vietnam | Masan High-Tech Materials (Nui Phao) | ~5,000 t WO₃ | Largest non-China primary tungsten mine |

Thailand | Multiple small producers | Variable | Au Club origin; FOB Laem Chabang |

Malaysia | Small mines | Modest | Au Club origin |

Bolivia | Several mines | Modest | Through Pacific ports |

Portugal | Beralt Tin and Wolfram | Modest | EU buyers |

Spain | Barruecopardo | Modest | EU buyers |

Russia | OMG, Tyrnyauz | Significant | Sanctioned for US/UK direct sale |

Australia | EQ Resources (Mt Carbine) | Growing | Restart phase |

Non-Chinese molybdenum

Country | Producer | Approx share | Notes |

Chile | Codelco, Antofagasta | ~20% | By-product, scale, captive |

US | Freeport (Henderson, Climax) | ~15% | Primary mines + Cu by-product |

Peru | Southern Copper, others | ~10% | Cu by-product |

Mexico | Mexicana Cananea | ~5% | Cu by-product |

Iran | NICICO | ~3% | Sanctions complications |

Mongolia | Erdenet | ~3% | Cu by-product |

Armenia | Zangezur | ~2% | Cu by-product |

Au Club supplies molybdenum oxide (MoO₃, 63% Mo minimum) with 300 MT/month availability and tungsten concentrate (55–65% WO₃) from Thailand and Malaysia. Tungsten scrap — both carbide and soft scrap — is sourced regionally and is a meaningful partial hedge for cutting-tool buyers facing APT shortages.

How to position your supply book

Three actions worth taking now:

- Audit your 2025-2026 forward contracts. If your existing supplier is Chinese — directly or via a smelter that aggregates Chinese ore — your contract is exposed to licence non-approval.

- Open a relationship with at least one non-Chinese supplier. Even at higher unit cost. The option value of having a working non-China channel exceeds the price premium.

- For tungsten carbide buyers, evaluate scrap. Tungsten carbide scrap can be re-processed into APT or used directly in some applications. Scrap pricing has tracked APT closely but with more available volume.

For very large buyers, multi-year offtake agreements with non-Chinese producers (Masan, Codelco, Freeport, EQ Resources) are now more accessible than they were in 2023 because Western producers are looking for non-China end-market commitments.

Au Club’s read

Tungsten and molybdenum are not going to retrace to pre-February 2025 levels in any realistic 2025 scenario. Our working range for European APT through 2025 is $420-520 per MTU WO₃. For US moly, $50,000-$60,000 per MT. The downside scenario — large MOFCOM approval wave — requires a US-China trade agreement that has not been signalled at any working level.

What we are telling buyers: do not wait for clarity. The clarity, when it comes, will come in the form of further escalation or a long, quiet plateau at higher prices. Build your non-China book now.

FAQs

Are tungsten exports from China actually banned?

No. They are under a licensing regime. The practical effect — based on the antimony precedent and limited approved licences since 4 February 2025 — has been a sharp reduction in Chinese tungsten export flow. Whether this constitutes a de facto embargo depends on MOFCOM’s approval rate over time.

Where can I source non-Chinese tungsten?

Vietnam (Masan Nui Phao), Thailand, Malaysia, Bolivia, Portugal, Spain, and (when sanctioned imports clear) Russia. Australia (Mt Carbine) is restarting commercial production. Au Club supplies concentrate from Thailand and Malaysia, plus tungsten scrap.

Is tungsten carbide scrap a viable substitute for APT?

For many cutting-tool re-manufacturing applications, yes. Scrap re-processing into APT is established technology. The economics work when APT prices are this elevated. Au Club buys and sells both carbide and soft tungsten scrap.

Will the price come back down?

Au Club’s working view is no, not in 2025. A return to early-2024 prices requires a meaningful US-China trade agreement and a clear MOFCOM approval pattern, neither of which has been signalled.

About Au Club

Au Club is a Dubai-based commodity trading company specialising in metals, minerals, and marine fuels. We supply tungsten concentrate (55-65% WO₃) from Thailand and Malaysia, tungsten scrap (carbide and soft), and molybdenum oxide (MoO₃ 63% Mo minimum). SGS or Alex Stewart pre-shipment inspection. LC and TT accepted. Contact our trading desk.