Copper Treatment Charges Hit Zero. Smelter Pain Is the Cathode Buyer’s Problem.

The 2026 annual copper TC/RC benchmark is being negotiated at or near $0 per metric ton — an unprecedented level. Smelters are paying for the privilege of refining concentrate. The cause is straightforward: Chinese sm…

The 2026 annual copper TC/RC benchmark is being negotiated at or near $0 per metric ton — an unprecedented level. Smelters are paying for the privilege of refining concentrate. The cause is straightforward: Chinese smelter capacity additions over the past five years have run ahead of global concentrate supply growth, and Chinese smelters now account for over 90% of growth in global copper output. For cathode buyers outside China, that has translated into record LME prices and tight prompt availability of LME-registered Grade A material. This article explains the mechanism, the numbers, and the procurement implications for 2026 cathode buyers.

What TC/RC is and why $0 matters

Copper smelters do not produce copper from ore. They produce copper cathode from concentrate — typically 25-30% Cu material delivered from mines. The smelter’s revenue model has two parts:

- By-product credits. Gold, silver, molybdenum, and sulphuric acid produced as by-products of copper refining.

- Treatment and refining charges. A fee per ton of concentrate processed (TC, treatment charge) and per pound of payable copper refined (RC, refining charge). These are deducted from the mine’s gross revenue and paid to the smelter.

For thirty years TC/RCs have functioned as the global pricing mechanism for the concentrate market. When concentrate is scarce, smelters bid each other down to win tonnage — TC/RCs fall. When concentrate is abundant, TC/RCs rise.

The annual benchmark TC/RC is negotiated each year between Freeport-McMoRan (or another major Western miner) and a Chinese or Japanese smelter. The 2024 benchmark settled at $80/MT. The 2025 spot has run as low as the $20s. The 2026 benchmark is being negotiated at or near $0.

$0 is not a normal price level. It signals that smelters are willing to accept zero processing fee — or even pay miners — to keep their furnaces loaded. That has happened in moments of acute concentrate scarcity (China’s industrial growth phase in the early 2000s); $0 as a sustained benchmark is genuinely new.

What is causing this

Three structural forces are at work:

1. Chinese smelter capacity has run ahead of concentrate

Between 2015 and 2025, Chinese refined copper output approximately doubled. New smelters at Tongling, Jiangxi, Yangzhou, Yantai, and several other locations brought online substantial new capacity. China’s share of global smelter output rose from approximately 15% to nearly 50% over the decade.

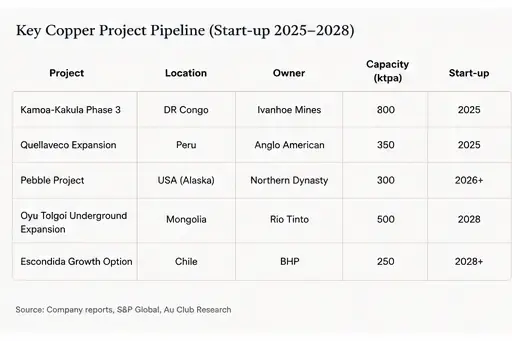

Mine supply did not keep pace. Major new projects (Quellaveco in Peru, Kamoa-Kakula in DRC) added supply, but project delays at Las Bambas (Peru), Cobre Panamá (Panama, closed since November 2023), and Mongolia’s Oyu Tolgoi underground expansion limited the upside.

The structural shortfall: too much smelter, not enough concentrate. Smelter competition for concentrate drives TC/RCs down.

2. The Cobre Panamá closure removed material supply

First Quantum’s Cobre Panamá mine was producing approximately 350,000 MT/year of copper-in-concentrate when the Panamanian Supreme Court ordered closure in November 2023. The mine has not restarted. That removed roughly 1.5% of global mine supply at a moment when smelter capacity was still growing.

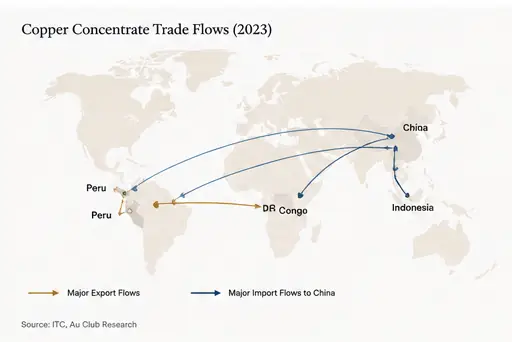

3. DRC quotas constrain growth

The DRC was the fastest-growing copper producer in the world through 2023. In early 2025 the government imposed export quotas (originally a ban, then a quota regime) that constrained the upside even when production was theoretically available. DRC Q1 2026 copper exports of approximately 955,000 MT were down 15% year-on-year from Q1 2025’s 1.09 million MT.

What this means for the LME copper price

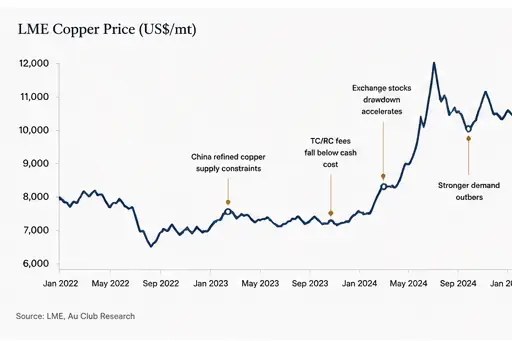

The LME three-month copper price has reacted accordingly. Through late 2025, the price climbed toward $13,000/MT and reached a record $14,527.50/MT on 29 January 2026. The forward curve has shown sustained backwardation — physical buyers paying a premium for prompt metal.

Period | LME 3-month copper ($/MT) |

Q1 2024 | $8,400 |

Q3 2024 | $9,200 |

Q1 2025 | $9,500 |

Q3 2025 | $11,200 |

Q4 2025 | $12,800 |

Late Jan 2026 (record) | $14,527.50 |

The price reflects the combination of mine supply constraints, smelter overcapacity, and accelerating demand from electrification and AI data centres. Electric vehicles, grid-scale transmission, and high-density compute infrastructure all rely on copper.

The unusual feature of this cycle is the simultaneity of high cathode prices and zero smelter profitability. In most cycles, high copper prices benefit smelters because by-product credits scale with copper revenue. This cycle, smelter margins have collapsed because they paid up for concentrate years ago and now compete with each other for shrinking supply.

Why LME Grade A cathode from non-China origins has become strategic

For Western cathode buyers — manufacturers of wire and cable, electric motors, transformers, busbars — the buying environment has changed in two ways:

- Prompt cathode availability outside China has tightened. Chinese smelters consume their own output, plus rising imports of concentrate from any available origin. The pool of cathode physically located outside China and registered to LME has shrunk in relative terms.

- Origin matters more than it used to. After the April 2024 LME ban on Russian-origin metal (see our August 2025 article on the one-year impact), non-Russian Grade A copper trades at a documented premium. Sanctioned-jurisdiction supply complicates the supply book of any large Western buyer.

Au Club’s LME Grade A copper cathode (99.99% Cu min) is sourced from Turkey and the UAE. Sarkuysan in Turkey produces LME-registered cathode at scale. Several UAE-based producers serve the Gulf and Asian markets. Both origins are clean from a sanctions perspective and from a sourcing-disclosure perspective.

Region | Major LME-registered brands | Notes |

Americas | Codelco (CCC, CMC), Freeport (FCX), Southern Copper | Captive offtake, premium pricing |

Europe | Aurubis, Boliden, KGHM | EU-priority offtake |

MENA | Sarkuysan (Turkey), various UAE | Au Club sourcing; growing market share |

Asia | Sumitomo, Mitsubishi, Tongling, JCM | Some Asia-bound, some restricted |

Africa | Glencore (Mutanda, KCC) | DRC quota-affected |

How to buy in a $0 TC/RC market

Three procurement adjustments worth making now:

1. Lock multi-year supply where possible. With cathode prices at record highs and forward curves in backwardation, the spot market is the worst place to be. Major Western consumers (cable manufacturers, electric motor producers) are signing 12-month, 24-month, and 36-month offtake agreements with Au Club and competitor traders. The premium for tenor is real but smaller than the spot volatility cost.

2. Diversify origin. A buyer with 100% supply from a single smelter is exposed to that smelter’s production disruptions, regulatory issues, and sanctions exposure. Aim for three or four origin relationships across two or three regions.

3. Negotiate premium structures. Cathode premium (the difference between physical price and LME) has widened. Codelco’s annual European premium for 2026 settled at multi-year highs. Premiums are not pure markup — they reflect physical scarcity. Engage on premium structure rather than just headline LME price.

Au Club’s offer

Au Club supplies LME Grade A copper cathode (99.99% Cu minimum) at 500-1,000 MT/month from Turkey and UAE producers. FOB terms. SGS or Intertek pre-shipment inspection. LC and TT payment. Full LME-registered brand documentation with each shipment.

For larger requirements (multi-year offtake agreements), the trading desk works directly with smelter relationships in Turkey, UAE, and selected European producers.

Looking ahead to 2027

The structural mismatch between Chinese smelter capacity and global concentrate supply is not resolving in 2026. New mine projects — Kamoa-Kakula expansions, Mongolian Oyu Tolgoi underground at full ramp, Indonesian copper from the Indonesian smelter build-out — will add supply in 2027-2028. But Chinese smelter capacity is also growing.

Two scenarios:

Base case. TC/RCs stay in single digits through 2026 and rise modestly in 2027 as new mine supply arrives. LME copper trades in a $11,000-14,000/MT range. Premiums remain elevated.

Bull case for buyers. A major Chinese smelter rationalisation. China has been signalling that it may consolidate or close inefficient smelter capacity. If 10-15% of Chinese smelter capacity exits the market, TC/RCs would normalise and physical premiums would compress.

For now, plan procurement around the base case.

FAQs

What is TC/RC?

Treatment Charge / Refining Charge — the fee a copper smelter charges a mine for processing concentrate into cathode. Quoted in dollars per metric ton of concentrate (TC) and cents per pound of payable copper (RC).

Why did TC/RC go to zero?

Chinese smelter capacity has expanded faster than global concentrate supply. Smelter competition for concentrate has bid TC/RC to zero — and in some spot transactions, to negative numbers.

Is cathode going to get more expensive?

The LME copper price has set successive records through 2025-2026. The structural drivers — electrification, AI data centres, mine supply constraints — suggest elevated prices through 2026 and likely 2027.

Where does Au Club source copper cathode?

LME Grade A from Turkey (Sarkuysan and others) and UAE producers. 500-1,000 MT/month availability. Non-Russian, non-sanctioned origin documentation with each shipment.

About Au Club

Au Club is a Dubai-based commodity trader supplying LME Grade A copper cathode (99.99% Cu minimum) from Turkey and the UAE. Multi-year supply structures available. SGS or Intertek inspection. LC and TT accepted. Contact our trading desk for current availability and pricing.