DRC, Mali, Indonesia: A 2026 Country-Risk Map for Critical Minerals Buyers

Resource nationalism stopped being a footnote in 2024. The DRC’s February 2025 cobalt export ban, Mali’s $1.2 billion mining-company arrears recovery, Indonesia’s confirmed plan to halt tin exports, and Burkina Faso’s…

Resource nationalism stopped being a footnote in 2024. The DRC’s February 2025 cobalt export ban, Mali’s $1.2 billion mining-company arrears recovery, Indonesia’s confirmed plan to halt tin exports, and Burkina Faso’s nationalisation push are not isolated stories. They are a co-ordinated shift in how producer states extract value from their mineral wealth. For commodity buyers, the implication is straightforward: country risk is no longer something to hedge against — it is a structural input to procurement strategy. This article scores ten producing jurisdictions on six risk dimensions and proposes contract clauses that hold up when policy shifts overnight.

The six country-risk dimensions that matter

A buyer evaluating country risk on a critical minerals purchase should assess six independent dimensions:

- Legal stability. Predictability of mining law, contract enforcement, and dispute resolution.

- Tax regime. Royalty rates, profit tax, windfall tax exposure, and the predictability of changes.

- Expropriation risk. Outright nationalisation or forced share transfer to state-owned entities.

- Currency convertibility. Ability to repatriate proceeds in USD or EUR at market rates.

- Logistics reliability. Port capacity, road and rail integrity, customs efficiency.

- Social licence. Community relations, indigenous land claims, labour stability.

Each dimension can be rated independently. Aggregate “country risk” is the combination — but no two buyers weight the dimensions identically. A defence supply chain weighs expropriation differently than a commercial trader weighs convertibility.

Heat-map: ten jurisdictions, six dimensions

Country | Legal | Tax | Expropriation | Currency | Logistics | Social licence | Aggregate |

DRC | Red | Amber | Amber | Red | Red | Amber | High |

Mali | Red | Red | Amber | Amber | Red | Amber | High |

Burkina Faso | Red | Amber | Red | Amber | Red | Red | High |

Indonesia | Amber | Amber | Amber | Amber | Amber | Amber | Medium-High |

Peru | Amber | Amber | Green | Green | Amber | Amber | Medium |

Chile | Green | Amber | Green | Green | Green | Amber | Low-Medium |

South Africa | Amber | Amber | Green | Amber | Red | Red | Medium-High |

Russia | Red | Red | Red | Red | Amber | Amber | High (sanctioned) |

Myanmar | Red | Red | Amber | Red | Red | Red | Very High |

Tajikistan | Amber | Amber | Amber | Amber | Amber | Amber | Medium |

The dominant pattern: the lowest-risk jurisdictions (Chile, Peru) are price-takers in tightly priced markets. The highest-risk jurisdictions (DRC, Mali, Burkina, Russia, Myanmar) host significant tonnage of strategic minerals. There is no clean way to source critical minerals at scale from only low-risk jurisdictions in 2026.

Three country deep-dives

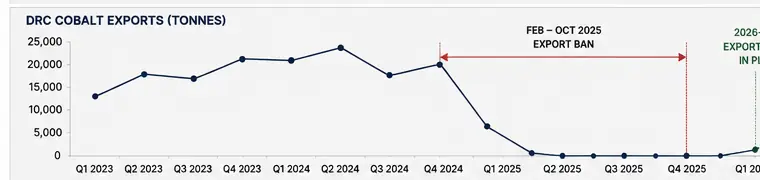

DRC: the February 2025 cobalt ban and October 2025 quota regime

The DRC produces approximately 70% of world cobalt, mostly as a copper by-product. In February 2025, the government imposed an outright export ban on cobalt concentrate. The stated rationale: build domestic refining capacity, capture more value, curb informal smuggling.

The ban created an immediate cobalt price spike (cobalt sulphate prices nearly doubled in Q1-Q2 2025) and severe disruption to refiners in China and Europe. In October 2025, the government lifted the ban but replaced it with a quota system: 18,125 MT for the remainder of 2025, then 96,600 MT/year for 2026 and 2027 — less than half of the DRC’s 2024 export volume.

The DRC also opened a copper export revenue audit, alleging revenue leakage in the export chain. Copper exports in Q1 2026 were down 15% year-on-year, reflecting some combination of quota effect, mine disruption, and audit-related delays.

The strategic takeaway for buyers: DRC supply is real but not reliable on a quarterly basis. Annual offtake agreements with major operators (Glencore, ERG, CMOC) are workable. Spot relationships are exposed to policy whiplash.

Mali: the $1.2 billion arrears recovery and the Barrick standoff

Mali’s military government has pursued an aggressive revenue strategy. The “Code Minier” revision raised royalty rates and applied retroactive assessments to existing mining operations. The government recovered approximately $1.2 billion in claimed arrears through audits and negotiations.

The Barrick Mining dispute is the highest-profile case. The Loulo-Gounkoto gold complex was disrupted by the dispute. Mali’s gold mine supply fell 19% in 2025 to approximately 81.2 metric tons. The disruption is meaningful for global gold supply at the margin.

Beyond gold, Mali hosts significant lithium and rare earth potential. The Goulamina lithium project is partially developed. The political environment makes new project financing difficult.

For commodity buyers: Mali is suitable for spot or short-tenor purchasing relationships, but locking multi-year supply is high-risk in the current political configuration.

Indonesia: the tin export-ban runway

Indonesia is the second-largest tin producer globally and accounts for approximately 25-30% of global refined supply. In 2024, refined tin exports collapsed to 46,000 MT — the lowest in two decades — driven by smelter seizures, RKAB (work plan) approval delays, and licence rationalisation.

In February 2026, Minister of Energy and Mineral Resources Bahlil Lahadalia confirmed government plans to halt tin exports entirely. The stated rationale mirrors the 2020 nickel export ban: force domestic value-addition before export. The 2020 nickel ban produced multi-billion-dollar investments in Indonesian smelter capacity and a ten-fold increase in nickel-product export value — the government cites this as the template.

Tin industry representatives have asked for phased implementation rather than immediate ban. Industry concerns include job losses (Bangka Belitung produces 91% of Indonesia’s tin and tin is 81.7% of provincial export value) and a sharp price spike that hurts domestic downstream consumers.

For tin buyers: Indonesian supply is not reliably available on a multi-year forward basis. Thailand (Au Club’s working origin) and Malaysia are the realistic alternatives. See Au Club’s October 2025 article on Thailand tin sourcing for working details.

The 2024-2026 resource nationalism timeline

A compact view of the major actions:

Date | Country | Action |

Aug 2024 | China | Antimony export licence regime |

Feb 2025 | China | Tungsten, moly, bismuth, indium, tellurium added to controls |

Feb 2025 | DRC | Cobalt export ban (10 months) |

Q1 2025 | Mali | Revenue arrears settlement; Barrick dispute |

Mar 2025 | Burkina Faso | Mining law revisions; state-stake increases |

Jul 2025 | US | Section 232 copper at 50% |

Sep 2025 | Indonesia | RKAB approval rationalisation |

Oct 2025 | DRC | Quota regime replaces ban (18,125 MT 2025; 96,600 MT/yr 2026-27) |

Feb 2026 | Indonesia | Confirmed plan to halt tin exports |

Q1 2026 | DRC | Copper export revenue audit |

Apr 2026 | US | Section 232 derivatives overhaul |

Not every action above is “resource nationalism” in the strictest sense — Section 232 is industrial policy by the importing country. But the cumulative effect on buyers is the same: governmental action is now a primary driver of commodity supply and price.

Contract clauses that hold up under policy whiplash

Three clauses worth getting right in any 2026 contract for high-risk-jurisdiction supply:

1. Force majeure scope. Generic FM language (“acts of government”) is insufficient. Specific events to include: – Export licence withdrawal or non-renewal at the origin country – Government-imposed quota changes – Mine closure order or operating-licence withdrawal – Sudden tariff or duty imposition by the destination country – Banking sanctions affecting payment or document presentation

2. Country-of-origin warranty. The seller warrants origin and provides documentation. The buyer has the right to inspect smelter records (with reasonable notice) and to reject shipments with non-conforming origin.

3. Pricing flexibility. Long-dated fixed-price contracts in high-risk-jurisdiction supply are dangerous. Floating reference (against an LME or Fastmarkets benchmark) is the safer structure. Multi-year contracts should permit annual re-pricing if origin-country royalty or tax changes shift the seller’s cost base.

Political-risk insurance

Several specialty insurers (Marsh, Aon, AIG, Sovereign, Chubb) write political-risk insurance covering:

- Currency inconvertibility

- Expropriation

- Political violence

- Trade-disruption events

Premia in 2025 range broadly: 0.3-1.2% of insured value per year for emerging-market trade financing, higher for jurisdiction-specific high-risk exposures. The cover pays out only when specific defined events occur; routine disruption (quota changes, licence delays) is typically excluded.

For large multi-year contracts, the premium can be material but justifiable. For routine spot purchases, the cost-benefit usually doesn’t work.

Au Club’s risk-management approach

Au Club operates in multiple high-risk jurisdictions (we source tin from Thailand, antimony from non-Chinese origins, fly ash from Kazakhstan, etc.). Three principles inform our approach:

- Diversified origin within each commodity. No single-origin exposure for any product line. Antimony from two non-Chinese origins; fly ash from four; tin from Thailand and Malaysia.

- Documentary discipline. Origin documentation is integrated into every shipment — not retro-fitted when a buyer asks.

- Transparency with buyers about risk. When a particular origin becomes harder to source from due to policy changes (Indonesian tin in 2025-2026, DRC cobalt in 2025), we tell customers explicitly rather than absorbing the risk silently.

For procurement teams: country risk is now a working input, not a tail risk. Score your suppliers, score your origins, build the resilience now.

FAQs

Which producing country has the highest current risk for commodity buyers?

By aggregate scoring, Myanmar, Russia (sanctioned), and Burkina Faso represent the highest current risk. DRC, Mali, and Indonesia are high-risk but more accessible in working contracts.

Did the DRC cobalt ban actually end?

The outright ban ended in October 2025. It was replaced with quotas: 18,125 MT for the rest of 2025, then 96,600 MT/year for 2026 and 2027 — substantially below 2024 export volumes.

Will Indonesia really ban tin exports?

Government statements (most recently February 2026) confirm the intention. Implementation timing is being negotiated. Industry representatives want phased introduction. The 2020 nickel-ban precedent suggests the government will follow through, though the exact date is uncertain.

Is political-risk insurance worth the cost?

For large multi-year contracts in high-risk jurisdictions, often yes. For routine spot purchases, the cost-benefit usually doesn’t justify the premium. Quote-shop multiple specialty insurers.

About Au Club

Au Club is a Dubai-based commodity trader. We source from multiple origins per commodity to manage country-risk concentration. Each shipment includes origin documentation and inspection certificates. Contact our trading desk for current sourcing options across your commodity requirements.