Inside the IMO Net-Zero Framework: A $500/MT Carbon Cost Is Coming to Marine Fuel

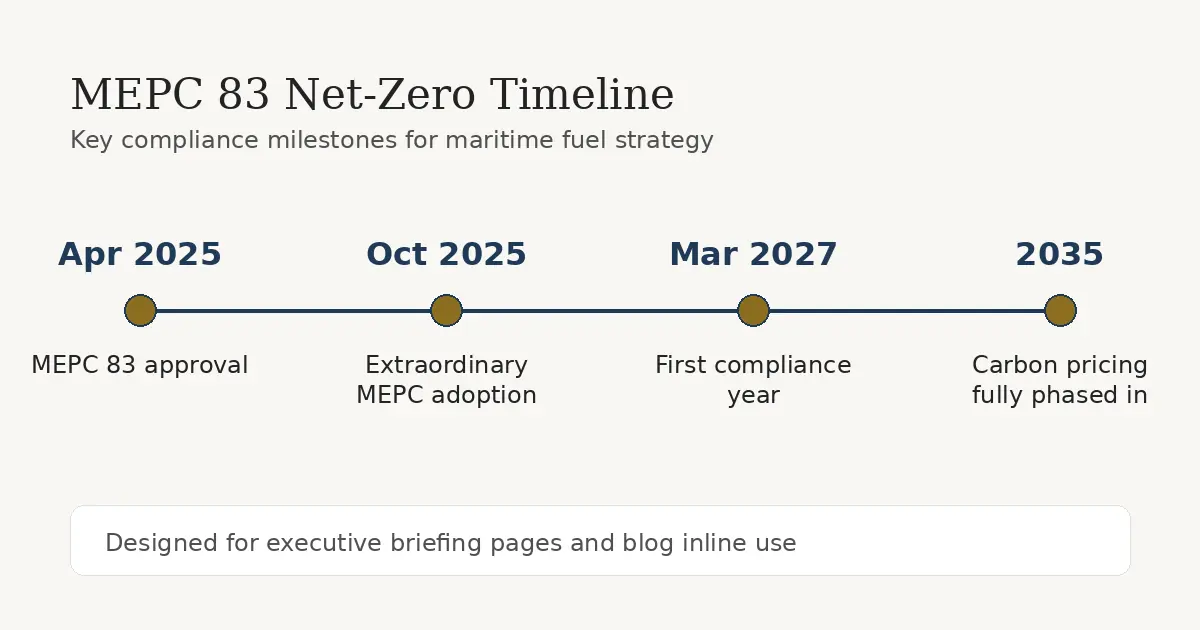

The IMO’s Marine Environment Protection Committee approved the Net-Zero Framework on 11 April 2025. It introduces a global carbon-pricing mechanism for ocean-going shipping over 5,000 GT, entering force on 1 March 202…

The IMO’s Marine Environment Protection Committee approved the Net-Zero Framework on 11 April 2025. It introduces a global carbon-pricing mechanism for ocean-going shipping over 5,000 GT, entering force on 1 March 2027. By 2035, vessels exceeding the GHG intensity target will pay up to $380 per ton of CO₂-equivalent for the worst-performing emissions — equivalent to roughly $500 per metric ton of conventional bunker fuel emitted above the base target. For a Suezmax tanker, that translates to several million dollars per year. For a 14,000-TEU container vessel, more. This is the operator’s guide to what was approved, what it means for 2027 bunker contracts, and what to do now.

What MEPC 83 approved

The 83rd session of the Marine Environment Protection Committee (7-11 April 2025) approved a goal-based fuel standard plus a global pricing mechanism for maritime GHG emissions. The framework applies to all ocean-going vessels over 5,000 GT, covering approximately 85% of global maritime emissions.

Two components:

Technical element. A goal-based marine fuel standard that progressively lowers the GHG intensity of marine fuels. Each year sets a target intensity in gCO₂e per MJ of energy delivered. The target tightens over time.

Economic element. A pricing mechanism for emissions. Vessels measure their actual GHG intensity on a well-to-wake basis (so emissions from fuel production count, not just combustion). Vessels that beat the target earn Surplus Units (SUs). Vessels that exceed the target either retire SUs from a previous compliance year, transfer SUs from other vessels in their fleet, or buy Remedial Units (RUs).

The RU is the priced unit. The IMO has set RU pricing tiers up to $380 per ton CO₂e for the deepest emission deficits by 2035 — translating to roughly $500 per metric ton of conventional bunker fuel above the base target.

The framework is due for formal adoption at an extraordinary MEPC session in October 2025. Adoption requires two-thirds of MARPOL Annex VI parties representing at least 50% of world tonnage. Once adopted, it enters force on 1 March 2027 with the first compliance year following.

The compliance band structure

MEPC 83 set two compliance tiers. The exact numbers will be confirmed at the October 2025 session, but the working structure is:

Tier | Compliance band | RU price (USD/tCO₂e) |

Direct compliance | At or below target intensity | $0 |

Base | Within tolerance band | $100 |

Advanced | Larger deficit | $380 |

The advanced-tier price is the headline figure. It is high enough to make even moderately above-target operations expensive, and high enough to materially favour LNG, methanol, biofuel, and (eventually) ammonia-fuelled vessels.

What this costs in practice

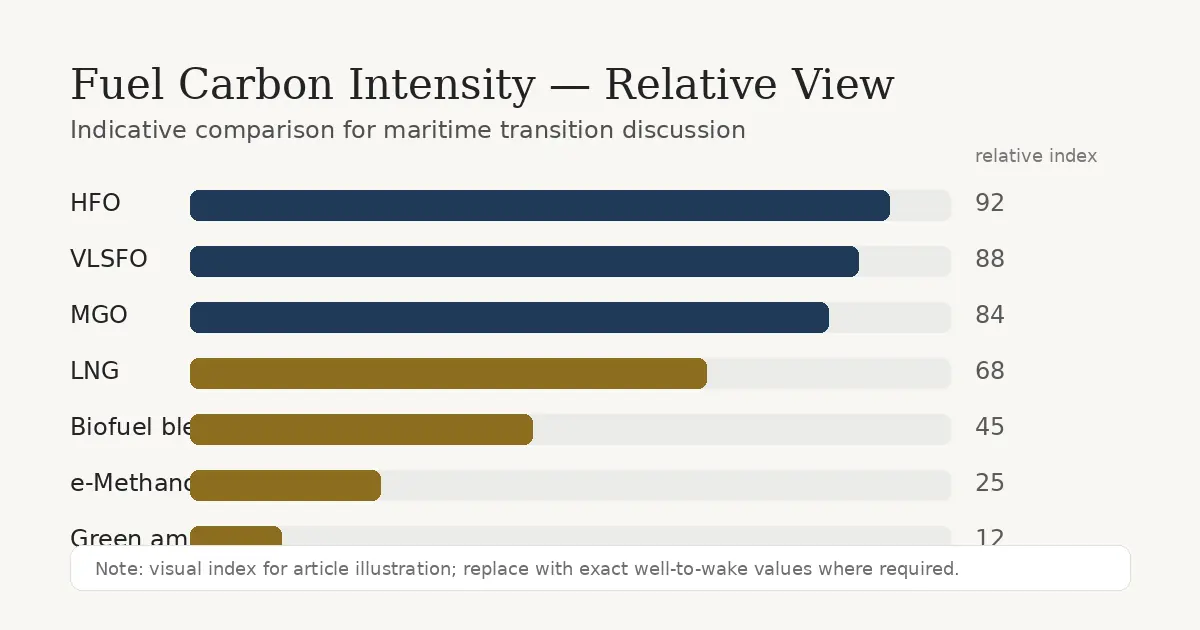

Worked example: 14,000-TEU container vessel, 32,000 MT/year bunker consumption, burning VLSFO at typical well-to-wake intensity of 91 gCO₂e/MJ. Target intensity in 2030 (illustrative): 75 gCO₂e/MJ.

Emission deficit per MJ delivered: 16 gCO₂e/MJ. At 40,000 MJ/kg energy content for VLSFO and 32,000 MT consumption, that is approximately 51,200 tCO₂e of deficit per year.

Year | Tier | RU price | Annual carbon cost |

2027 (first year, base tier) | Base | $100 | ~$5.1m |

2030 (deeper deficit, base tier) | Base | $100 | ~$7m |

2035 (advanced tier) | Advanced | $380 | ~$19.5m |

A 14,000-TEU vessel running on VLSFO faces $5m of carbon cost in year one of the framework. By 2035, if the vessel has not moved to lower-intensity fuel, the figure approaches $20m per vessel per year.

For a Suezmax tanker (14,000 MT bunker/year), scale down proportionally — but the absolute numbers are still meaningful for fleet economics.

How Surplus Units actually work

The Surplus Unit mechanism is the bridge from compliance to commercial reality. A vessel burning LNG might be running at 60 gCO₂e/MJ — well below the 75 target. It earns SUs equal to its annual surplus.

Three things an owner can do with SUs:

- Bank them for use in a future compliance year when their fleet might be above target

- Transfer them to another vessel in the same fleet (intra-fleet pooling)

- Sell them on the international market (the IMO is establishing the infrastructure)

The expected price of SUs sits between $0 (cost of compliance for over-performers) and the RU price. Active SU trading should compress prices toward the lower end of the range, but illiquidity in early years will likely keep SUs trading closer to RU prices.

The result is a real economic incentive for any fleet to have at least some alternative-fuel vessels. A mixed fleet of VLSFO and LNG can use the LNG SUs to offset some of the VLSFO RU obligations — improving overall fleet economics.

How MEPC 83 sits next to EU ETS and FuelEU Maritime

Two regional regulations already exist:

EU ETS for shipping — entered force 1 January 2024. Vessels calling at EU ports pay for 40% of CO₂ emissions in 2024, 70% in 2025, and 100% from 2026. Coverage applies to intra-EU voyages (100%) and extra-EU voyages calling at one EU port (50%).

FuelEU Maritime — entered force 1 January 2025. Imposes a GHG intensity standard on the energy used by ships calling at EU ports. Tightens 2% in 2025, then progressively to 80% by 2050.

MEPC 83 Net-Zero Framework — enters force 1 March 2027. Global scope. Covers vessels over 5,000 GT.

For an Asia-Europe operator, the three regulations stack:

Voyage | EU ETS | FuelEU | IMO Net-Zero |

Singapore-Rotterdam | 50% of CO₂ priced | Yes (intensity test) | Yes (full scope) |

Singapore-Houston | No | No | Yes (full scope) |

Hamburg-Antwerp | 100% of CO₂ priced | Yes | Yes |

EU ETS and FuelEU operate independently of the IMO framework, which means an EU-calling vessel pays the regional regimes on top of the global one. There is ongoing negotiation about how to avoid double-counting. The IMO and the European Commission have signalled flexibility but no clean solution has been agreed.

For now, expect 2027-2030 to involve overlapping compliance obligations and meaningful complexity in voyage planning.

What to write into 2026 charter parties and bunker contracts

For charterers — three clauses worth checking in any 2026 fixture:

- Carbon cost allocation. Who pays RUs and EU ETS? The CII Operations Clause for Time Charter Parties (BIMCO, 2022) was the first attempt; expect a 2026 update that addresses MEPC 83 specifically.

- Surplus Unit ownership. If a chartered LNG vessel generates SUs, do they belong to the owner or the charterer? Time-charter fixtures typically default to the owner unless explicitly assigned. Voyage charters usually keep them with the owner.

- Bunker stem flexibility. With MEPC 83 incentivising alternative fuels, charter parties should permit (not just allow) bunker stems of LNG, methanol, biofuel, or biofuel blends where compatible with the vessel’s machinery.

For bunker contracts, the Au Club desk is moving customers toward: – Fuel intensity certification at point of supply (well-to-tank documentation) – Biofuel blend specification (e.g., B30 means 30% biofuel content) where used – ISO 8217:2024 conformity (the standard now includes alternative fuels)

Au Club’s read on 2027 readiness

Three working positions:

- The framework will be adopted in October 2025. Indications from the April session were positive. Adoption is procedural rather than uncertain.

- VLSFO will remain the dominant fuel through 2027 and likely 2028. Alternative-fuel infrastructure is not at scale outside Singapore and a handful of European ports.

- Owners who do nothing in 2025-2026 will pay measurable RU bills from 2027 onward. That cost is going into operating expense, not capex. Even modest action (biofuel blends, route optimisation, hull cleaning, energy efficiency retrofits) reduces the bill.

For a fleet owner reading this in early 2025: the relevant question is not whether MEPC 83 will happen, but what mix of fuel, vessel efficiency, and SU acquisition makes financial sense for your specific fleet profile. The answer is different for a container owner than for a dry bulk owner; different again for tanker. Build the model now.

FAQs

When does the IMO Net-Zero Framework enter force?

1 March 2027, assuming adoption at the October 2025 extraordinary MEPC session.

Does MEPC 83 apply to my vessel?

If your vessel is over 5,000 GT and engaged in international voyages, yes. Domestic voyages within a single country are typically excluded.

How is GHG intensity measured?

On a well-to-wake basis — emissions from fuel production plus combustion. Measured in gCO₂e per MJ of energy delivered.

What is the maximum carbon price?

Up to $380 per ton CO₂e for the highest tier of non-compliance, equivalent to approximately $500 per ton of conventional bunker fuel above the base target. This is the 2035 figure; earlier years use lower prices.

Can I use biofuel to comply?

Yes — sustainable biofuels are recognised. The eligibility criteria for what counts as “sustainable” are still being refined. Biofuel blends like B30 (30% biofuel in HFO or VLSFO) are operational at Singapore and Rotterdam.

About Au Club

Au Club supplies VLSFO and HSFO at UAE ports with ISO 8217:2024 documentation. We work with customers on multi-year supply structures that anticipate MEPC 83 compliance obligations. Contact our bunker desk to discuss your 2026-2030 strategy.