Tin Concentrate Sourcing in 2026: Why Thailand Beats Indonesia on Reliability

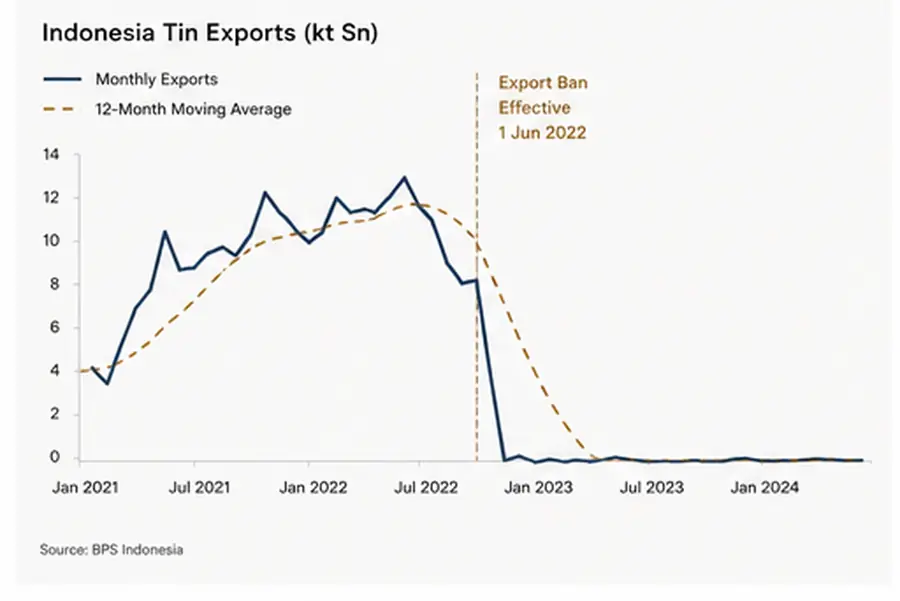

Indonesia’s refined tin exports collapsed to approximately 46,000 metric tons in 2024 — the lowest in more than twenty years. The country accounts for roughly 25-30% of world refined tin supply and the government has…

Indonesia’s refined tin exports collapsed to approximately 46,000 metric tons in 2024 — the lowest in more than twenty years. The country accounts for roughly 25-30% of world refined tin supply and the government has confirmed plans to halt exports entirely. For tin concentrate buyers — refineries, downstream solder manufacturers, electronics suppliers, tinplate producers — the procurement question for 2026 is no longer “Indonesia or somewhere else?” It is “where else, and how do I qualify the supply?” Thailand is the answer Au Club gives most customers. This is why, with the working details on specification, logistics, and contract structure.

Why Indonesia is no longer the default

Three structural problems hit Indonesian tin supply in 2024-2025:

1. Smelter confiscations. In 2024, the Attorney General’s Office confiscated five private tin smelters representing approximately half of Indonesia’s refining capacity. The investigations involved allegations of illegal mining and corruption. The seized facilities operated at reduced or zero output during 2024.

2. RKAB (work plan) delays. Indonesia requires mining companies to submit and obtain approval for annual production plans (RKAB). Through 2024-2025, RKAB approvals from the Resources Ministry and Trade Ministry were delayed, suspended, or scaled back. Even smelters that were not confiscated faced production caps.

3. Government export-ban intent. Minister of Energy and Mineral Resources Bahlil Lahadalia confirmed in February 2026 that the government intends to halt tin exports, replicating the 2020 nickel export ban model. Implementation timing is uncertain but the policy direction is clear.

The cumulative effect: 2024 refined exports of 46,000 MT was approximately half the 2020 baseline. 2025 trends are similar. 2026-2027 are uncertain.

What this does to global tin supply

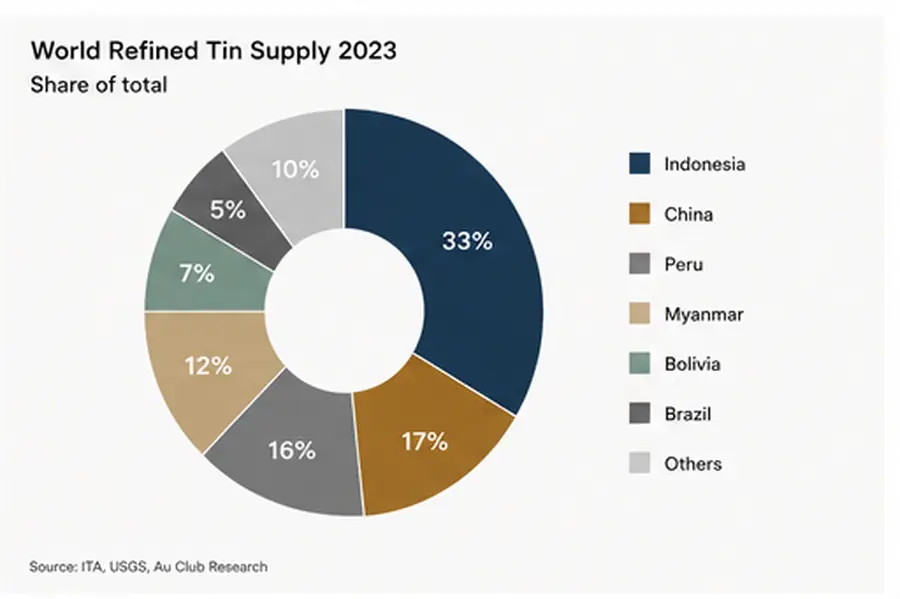

World tin mine production in 2023 was approximately 290,000-310,000 MT (estimates vary by source). Indonesia historically supplied 80,000-90,000 MT. China is the largest producer at approximately 80,000-100,000 MT. Then Myanmar (volatile, approximately 30,000-50,000 MT), Peru, Bolivia, Australia, DRC, Nigeria, and Thailand round out the supply base.

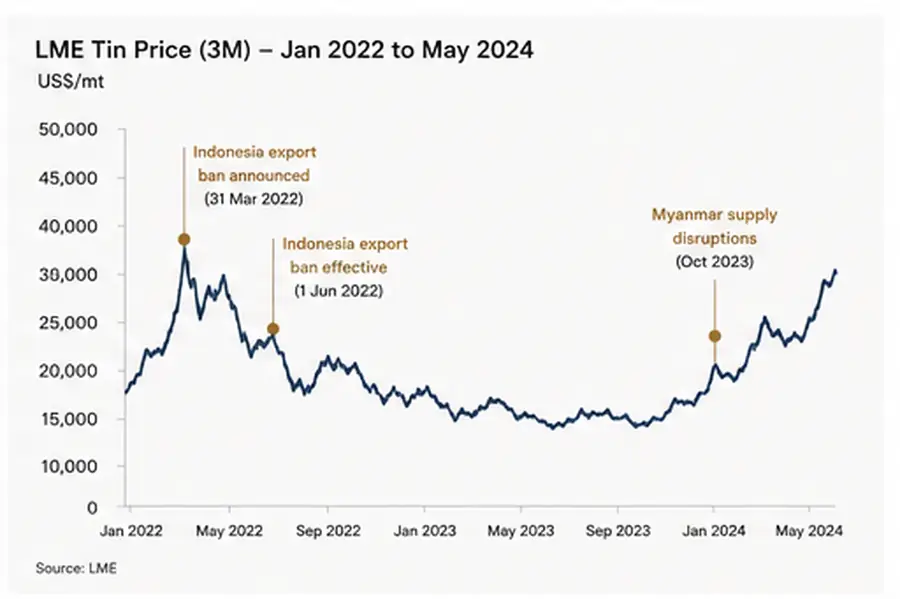

When Indonesia withdraws even 30,000-40,000 MT, the market scrambles. LME tin prices reflected this through 2024 and 2025: ranging from $25,000 to $35,000 per metric ton, well above the pre-2020 averages of $18,000-22,000.

For concentrate buyers (refineries), the question is not just price but availability. The Indonesian disruption pushed refineries to qualify new origin relationships.

Thailand’s tin profile

Thailand has been a tin producer since the 19th century. Modern Thai production is smaller than peak years (which exceeded 100,000 MT in the 1970s) but remains commercially meaningful. Current annual mine output is in the range of 8,000-15,000 MT, with the variability driven by artisanal and small-mine activity rather than primary industrial operations.

The Thai tin chain has three distinct stages:

- Mining. Predominantly small-scale and artisanal, with significant operations in Phuket, Phangnga, and Ranong provinces. Some industrial operations exist but the majority is independent producer-aggregator activity.

- Concentrate consolidation. Aggregators consolidate concentrate from multiple small producers, blend to target Sn content, and present to smelters or to international export buyers.

- Export. FOB Laem Chabang for container shipment; FOB Bangkok for break-bulk.

Thailand’s advantage for international buyers is structural reliability rather than scale. The legal environment is stable. The aggregator infrastructure is established. The export route through Laem Chabang is direct and efficient. The currency (Thai Baht) is convertible. The Thai government is not pursuing export restrictions.

Specification: 40-70% Sn concentrate

Tin concentrate sold internationally is graded by tin content:

Grade | Sn content | Typical buyer | Key impurities to monitor |

Low-grade | 40-50% Sn | Smelters with flexible feed | As (arsenic), Fe (iron), Pb (lead) |

Mid-grade | 50-60% Sn | Standard refinery feed | As, Fe, Pb, S (sulphur) |

High-grade | 60-70% Sn | Premium refineries | As, Fe, Pb, low S preferred |

A typical Thai concentrate Au Club moves into international markets sits in the 55-65% Sn range. Higher Sn content commands a higher price per dry metric ton, but the relationship is not linear — penalty schedules for impurities (especially arsenic, which raises smelting costs and environmental compliance burden) can affect the net realised price.

The Thai concentrate Au Club handles typically meets:

- Sn: 55-65% (specified per shipment)

- As: ≤ 0.5% (lower preferred)

- Fe: ≤ 5%

- Pb: ≤ 1%

- S: ≤ 2%

- Moisture: ≤ 5% at loading

Pre-shipment inspection is by SGS or Alex Stewart. Each shipment carries a Certificate of Analysis with chemistry, moisture, and weight.

Logistics: FOB Laem Chabang

The working logistics:

Loading port. Laem Chabang, approximately 2 hours by road south of Bangkok. Major container terminal with established mineral concentrate handling. Some shipments load at Bangkok or other Thai ports for break-bulk, but container shipment from Laem Chabang is the standard for international buyers.

Vessel sizing. Tin concentrate is high-value and low-volume per unit. Most shipments move in containers (20-foot, 25-30 MT per container) rather than break-bulk vessels. Lot sizes typically 50-300 MT.

Lead times. From order confirmation to FOB Laem Chabang typically 30-45 days, depending on aggregation cycle. Ocean transit to Gulf ports approximately 18-25 days. To European ports 30-35 days. To Asian destinations (China, Japan, Korea) 7-14 days.

LME tin price reference. Most concentrate contracts price as a discount to LME tin three-month, with the discount reflecting Sn content, impurity penalties, and smelter treatment charges. A typical 60% Sn concentrate might price at LME three-month tin minus 20-25% (representing the contained tin payable, treatment charges, and impurity penalties).

Malaysia and Myanmar as secondary origins

Two other origins Au Club tracks:

Malaysia. Historical tin producer with a small but consistent modern output. Pricing and reliability comparable to Thailand. FOB Port Klang. Volumes smaller than Thai aggregators.

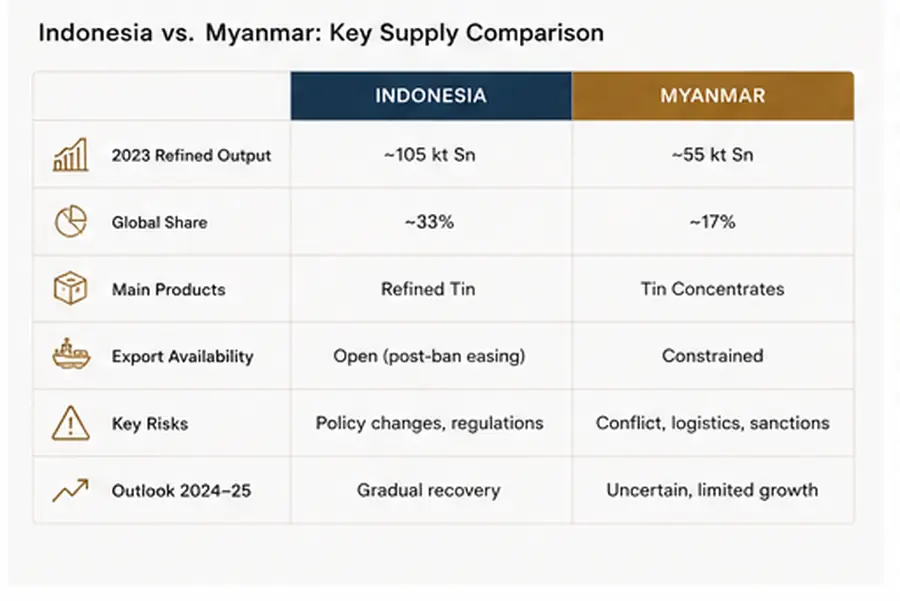

Myanmar. A meaningful tin producer, but with three constraints. First, much Myanmar tin output is informal and concentrated in the Wa State region under unclear governance. Second, supply has been volatile, with significant interruptions in 2023 from operational disruptions. Third, US sanctions on Myanmar military entities complicate buyer compliance. Some buyers source Myanmar tin successfully; many compliance regimes flag it.

For buyers prioritising clean documentation and predictable supply, Thailand is the more accessible origin.

How an Au Club tin concentrate contract is structured

Standard terms for a refinery buyer:

- Volume. Per enquiry, typically 50-500 MT per shipment, with annual offtake commitments possible.

- Sn content. 40-70% (specified per shipment).

- Origin. Thailand (primary), Malaysia (secondary).

- Loading port. Laem Chabang (Thailand) or Port Klang (Malaysia).

- Inspection. SGS or Alex Stewart at loading.

- Documentation. COA, COO, BL, packing list, inspection certificate.

- Price formula. LME three-month tin minus negotiated treatment charge and impurity penalties. Fixed price available for shorter contracts.

- Payment. LC at sight, deferred LC (30/60/90 days), or TT against documents. Most international refineries use LC.

For first-time buyers, Au Club typically offers a single-shipment trial (50-100 MT) to allow the refinery to qualify the concentrate against its smelting process. Successful trial shipments lead to monthly or quarterly offtake.

Au Club’s read for 2026

Three working positions:

- Indonesian supply remains unreliable through 2026. Whether or not the formal export ban implements on schedule, Indonesian tin in the international market will be intermittent and unpredictable. Plan around it, not for it.

- Thai supply has structural headroom. Existing aggregator infrastructure can absorb additional buyer demand without disruptive price moves. 2026 supply is available for refineries willing to engage on contract structure.

- LME tin trades in $28,000-38,000/MT range through 2026. The Indonesian uncertainty puts a floor under price; new supply ramp from secondary origins keeps a ceiling on speculative spikes.

For refineries and downstream tin buyers: qualify a Thailand origin now. The cost of qualifying a new supply chain is meaningful — sample analysis, smelter trials, documentation discipline — but it is much smaller than the cost of being short of feed when Indonesian shipments don’t arrive.

FAQs

Is Indonesia really going to ban tin exports?

The government has confirmed the intention as recently as February 2026. Implementation timing is being negotiated. Industry representatives are pushing for phased introduction. The 2020 nickel-ban precedent suggests the government will follow through.

Where is the world’s tin produced?

China (~30%), Indonesia (~25-30% in normal years), Myanmar (~10-15%), Peru, Bolivia, Australia, DRC, Thailand, Nigeria, Malaysia, Vietnam, Russia. Production concentration is meaningful but less than tungsten or cobalt.

What is the current price of tin concentrate?

Tin concentrate prices reference the LME three-month tin price, discounted for treatment charges, impurity penalties, and contained tin payable. As of late 2025, LME tin three-month is in the $30,000/MT area. Concentrate at 60% Sn might price at approximately 75% of contained tin value.

Does Au Club handle Myanmar-origin tin?

Au Club’s primary tin origins are Thailand and Malaysia. We can discuss Myanmar concentrate for specific buyer requirements, with the compliance and provenance documentation that entails.

About Au Club

Au Club supplies tin concentrate (40-70% Sn) from Thailand and Malaysia, FOB Laem Chabang or Port Klang. SGS or Alex Stewart pre-shipment inspection. LC and TT accepted. Contact our trading desk for sample analysis, trial shipments, and 2026 offtake arrangements.