One Year After the LME Russian Metals Ban: Origin Now Trades at a Premium

On 12 April 2024, the US Treasury and the UK Government announced parallel restrictions on Russian-origin aluminium, copper, and nickel produced from 13 April onwards. Sixteen months later, the immediate market reacti…

On 12 April 2024, the US Treasury and the UK Government announced parallel restrictions on Russian-origin aluminium, copper, and nickel produced from 13 April onwards. Sixteen months later, the immediate market reactions — aluminium spiking 9.4% in a single day, the LME and CME re-papering warehouse stocks — have given way to a more interesting structural picture. Documentary origin now trades at a measurable premium. LME warehouse composition has shifted. And buyers writing 2026 contracts cannot treat origin as a tick-box exercise. Here is what changed, what stuck, and what buyers should be doing now.

What was banned and what was grandfathered

The 12 April 2024 announcement was carefully constructed. The restrictions did not ban Russian-origin metal outright. They banned:

- Import to the US and UK of Russian-origin aluminium, copper, and nickel produced on or after 13 April 2024.

- New LME and CME warrants from Russian metal produced on or after 13 April 2024.

Critically, Russian-origin metal produced before 13 April 2024 remained eligible for LME warranting. That created a two-tier market: pre-ban Russian metal could continue to trade on the LME, while post-ban Russian metal could not.

The LME’s own rules went further. In April 2024, the LME introduced restrictions on the ability of Russian-origin metal to be delivered against new LME contracts, while maintaining warrant validity for pre-existing stocks. Subsequent rule refinements addressed potential “gaming” — moving Russian-origin metal between warehouses to extend its tradeability.

The result was a complex and evolving rulebook that traders, brokers, and warehouse operators have been navigating for sixteen months.

Pre-ban warehouse composition

The immediate stock backdrop was striking. Before the 12 April announcement, Russian metal dominated LME warrant stocks:

Metal | Pre-ban LME warehouse share (March 2024) |

Aluminium | ~91% Russian-origin |

Copper | ~62% Russian-origin |

Nickel | Significant share (composition less concentrated) |

These shares reflected years of accumulation. Russian primary aluminium producer Rusal had been the dominant warrant supplier to LME warehouses for over a decade. Russian copper from UMMC and the Russian Copper Company similarly built up.

When the ban took effect, this pre-ban stock did not disappear. It remained in LME warehouses, eligible for re-warranting under the rules, and continued to trade. The new prohibition applied only to post-13-April production.

The immediate market reaction

The 12-19 April 2024 price reaction was dramatic but short-lived:

Metal | Day-after move | One-week move | One-month move |

Aluminium | +9.4% (highest single-day move since 1987) | +4% | -1% |

Copper | +2.5% | +1% | +0.5% |

Nickel | +8.8% | +5% | -3% |

The initial spike priced in worst-case supply scenarios. As traders worked out the grandfather clause and the pre-ban warrant pool, prices normalised. By mid-May 2024, headline LME prices had largely retraced.

But underneath the headline, three more durable effects took hold.

The three durable effects

1. Russian-origin metal moved off-warrant

Most Russian-origin post-13-April production has gone to non-LME-warrant destinations — primarily China, Turkey, the UAE, and selected MENA re-export markets. China imports of Russian aluminium and copper rose substantially through 2024 and 2025.

This means the headline ban achieved part of its objective: Russian revenue from Western markets dropped meaningfully. But globally, Russian metal continues to flow at near-pre-ban volumes — just to different buyers.

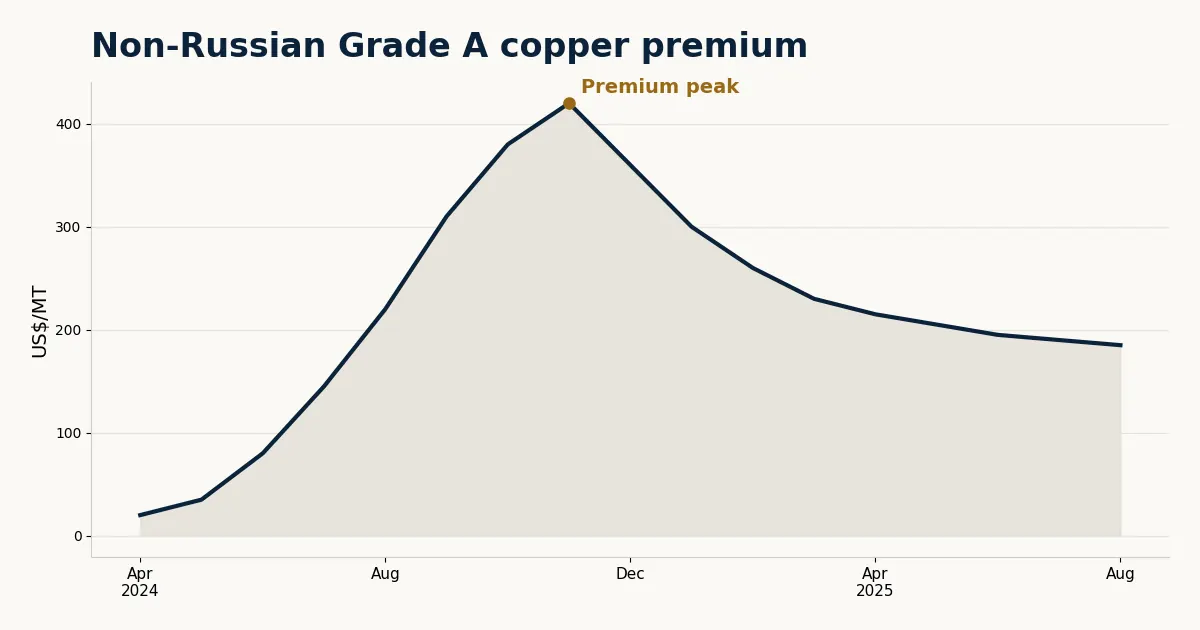

2. A documentary-origin premium emerged and persists

Non-Russian Grade A copper, P1020 aluminium, and Class 1 nickel now trade at a measurable premium to Russian-origin equivalent. The premium varies by metal:

Metal | Non-Russian premium (approx, mid-2025) |

Aluminium P1020 | $40-90/MT over Russian-equivalent off-warrant prices |

Copper Grade A | $25-60/MT |

Nickel Class 1 | $200-450/MT |

For aluminium, the premium widened sharply in April 2024 and narrowed somewhat through 2024-2025 as the market adjusted. For copper, the premium has been more stable. For nickel, the premium reflects the metal’s smaller market and concentration of non-Russian supply (Indonesia, Australia, New Caledonia).

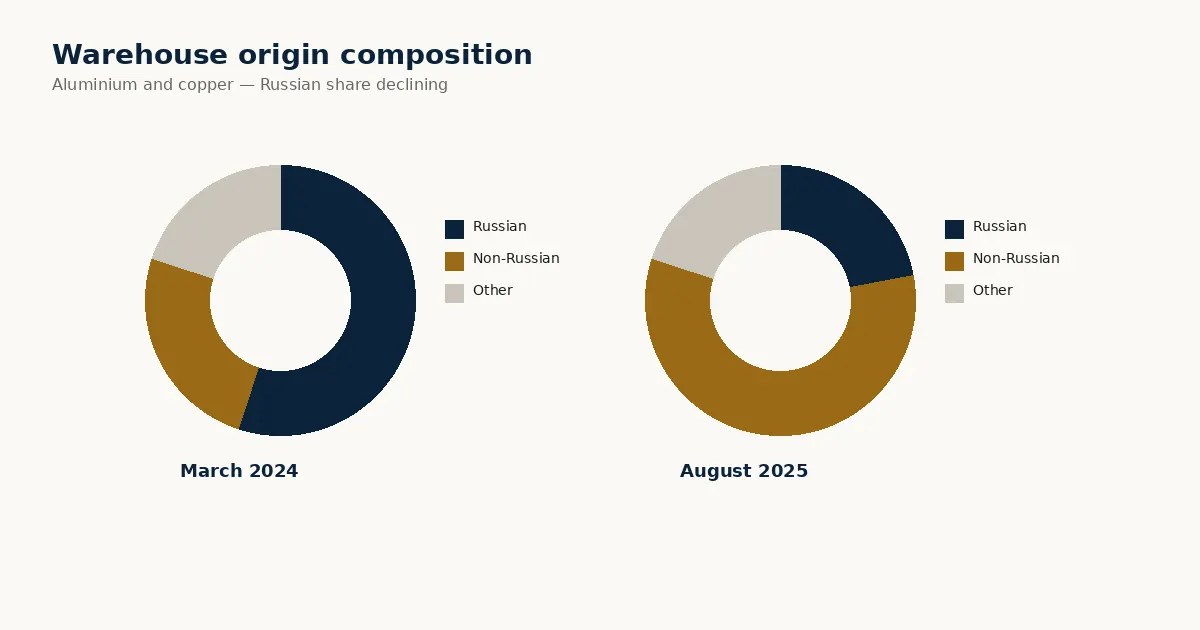

3. LME warehouse composition shifted

By August 2025, LME warehouse composition had changed materially from the pre-ban baseline:

Metal | LME warehouse Russian share (March 2024) | LME warehouse Russian share (Aug 2025) |

Aluminium | ~91% | ~78% |

Copper | ~62% | ~38% |

The shift reflects pre-ban Russian metal being drawn down through trading, with new warrants coming predominantly from non-Russian sources. The pre-ban Russian stocks will continue declining as physical buyers draw them down for delivery.

What documentary requirements actually look like in 2025

For a buyer wanting confirmed non-Russian origin, the working documentation set:

1. Certificate of Origin (COO). Issued by the chamber of commerce of the producing country. References the smelter and the country of production.

2. Mill Test Certificate (MTC) or Certificate of Analysis (COA). From the smelter, listing chemical composition and the heat / lot number. Cross-references to the LME registered brand if applicable.

3. LME Warrant (if buying on warrant). Specifies the warehouse, the brand, and the production date. The combination of brand and date establishes whether the metal is pre-ban or post-ban Russian (subject to LME rule eligibility).

4. Smelter declaration. Some sophisticated buyers ask for a direct smelter declaration confirming country of melt and country of pour. This is becoming standard for defence-adjacent applications.

5. Sanctions screening. The buyer’s bank and the LC-confirming bank screen the smelter, the country, and the registered brand against OFAC SDN list, UK HMT consolidated list, and EU Council Regulation lists.

For a contract drafted in 2023, much of this was implicit. For a contract drafted in 2025, it should be explicit.

How to draft an origin clause that holds up

Three elements that should appear in any 2026 contract:

Specific exclusion language. Not “non-sanctioned origin” (vague) but “Russian-origin metal, including metal produced at any smelter located in the Russian Federation or by any entity owned 50% or more by a Russian person or entity, is excluded.” Reference applicable OFAC/HMT/EU regulations by name.

Documentation chain of custody. Specify required documents at each transfer point (loading port, in-transit, discharge port). Specify that failure to produce these documents triggers buyer’s right to reject without penalty.

Audit right. Buyer’s right to inspect, with reasonable notice, the supplier’s smelter relationships and origin documentation. This is the clause sophisticated buyers add and most suppliers accept.

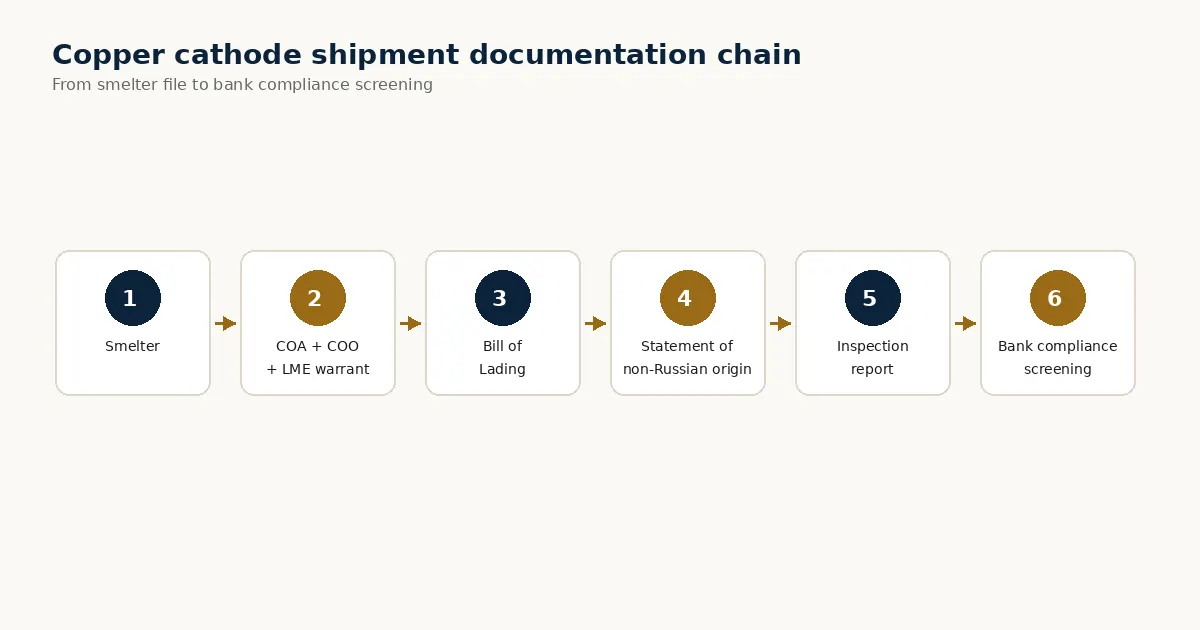

Au Club’s documentation approach

Au Club’s standard cathode shipment includes:

- COA from the smelter

- Certificate of Origin from the host chamber of commerce

- LME warrant where applicable

- Bill of Lading and Packing List

- Statement of non-Russian origin (separate document, signed by Au Club)

- Inspection report by SGS or Intertek

The Au Club statement of non-Russian origin is a standing document for our Turkey and UAE sourcing. It is reissued per shipment, dated, and includes the smelter name and production reference. This is the document our buyers’ compliance teams cite when their banks ask for confirmation.

Au Club’s read for 2026

Three working positions:

- The ban does not get rolled back in 2026. A Russia-Ukraine settlement might trigger phased relief, but no major Western jurisdiction has signalled relaxation of the metals restrictions.

- The origin premium persists at current levels or modestly widens. Documentary scrutiny is increasing, not decreasing. Premium for confirmed origin reflects real compliance cost — not pure scarcity.

- Pre-ban Russian warrant stock will deplete by mid-2027. The pool of pre-13-April-2024 Russian metal in LME warehouses is finite. As it depletes, the LME composition will shift further to non-Russian sources. By 2027, the Russian share of LME aluminium warrants will likely fall below 50%.

For buyers writing 2026 supply contracts: get the origin documentation explicit, build buffer for documentation-related delays at customs, and budget the non-Russian premium into your annual procurement.

FAQs

Can I still buy Russian-origin copper on the LME?

Russian-origin metal produced before 13 April 2024 remains eligible for LME warrants and can trade. Post-13-April production cannot be newly warranted on the LME or CME. The pre-ban stocks are gradually depleting.

What is the premium for non-Russian Grade A copper?

Approximately $25-60/MT over Russian-equivalent off-warrant pricing in mid-2025. The premium is most pronounced for buyers with strict sanctions screening requirements (defence, US/UK government suppliers).

Does Au Club handle Russian-origin material?

No. Au Club’s Turkey and UAE cathode sources are non-Russian. We provide a statement of non-Russian origin with each shipment.

Will the LME ban be lifted?

Not in any near-term scenario. A future political settlement on Russia-Ukraine could trigger phased relief, but no major Western jurisdiction has signalled that.

About Au Club

Au Club supplies non-Russian-origin LME Grade A copper cathode (99.99% Cu min) from Turkey and the UAE. Each shipment includes full origin documentation, smelter-of-origin attestation, and SGS or Intertek pre-shipment inspection. Contact our trading desk to discuss compliant supply for your 2026 requirement.