Section 232 Goes Global: Trump’s 50% Copper Tariff and the Gulf Trade Flow

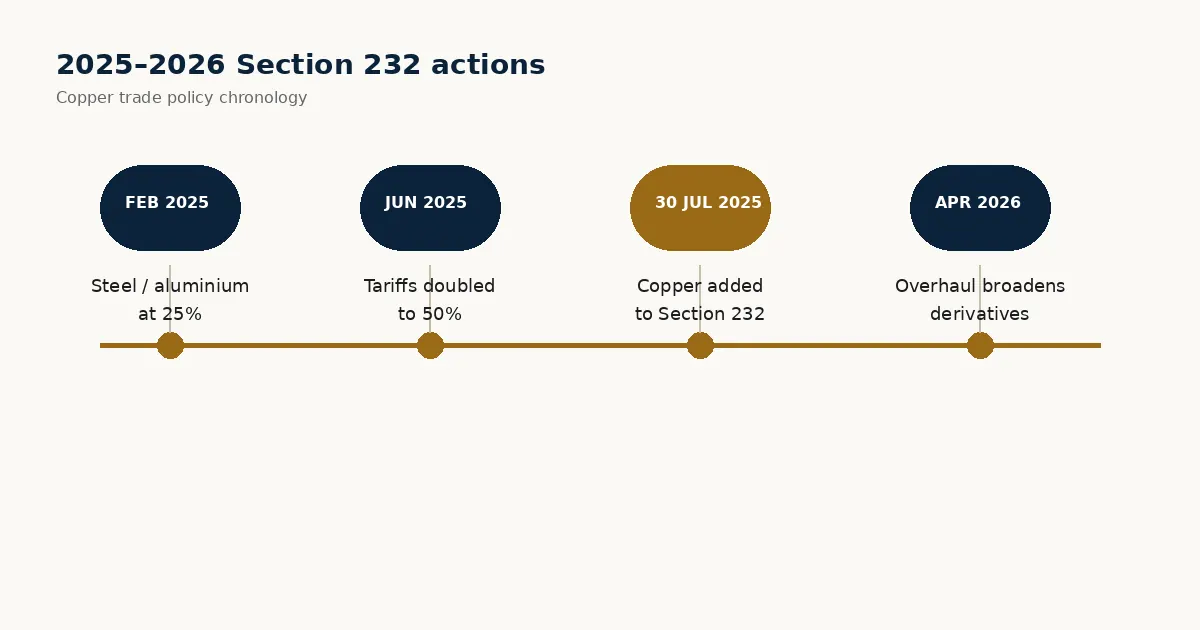

On 30 July 2025 the White House added copper to the Section 232 tariff list at 50%, matching the rates on steel and aluminium. For Gulf-based copper cathode suppliers, the immediate effect was a sharp drop in US-bound…

On 30 July 2025 the White House added copper to the Section 232 tariff list at 50%, matching the rates on steel and aluminium. For Gulf-based copper cathode suppliers, the immediate effect was a sharp drop in US-bound demand and a parallel widening of arbitrage opportunities into Asia and Europe. For US-based industrial buyers, the effect is a 50% landed-cost increase on imported cathode that, in 2024, supplied roughly half of US copper consumption. This article maps the regulatory chronology, the trade-flow consequences, and the contractual adjustments Au Club’s customers are making for 2026.

How we got here: the 2025 chronology

The Trump administration’s second-term Section 232 programme has moved fast:

- February 2025: Steel and aluminium Section 232 tariffs reimposed at 25%. Most country-specific exemptions and product-specific exceptions eliminated.

- June 2025: Steel and aluminium rates doubled to 50%.

- 30 July 2025: Copper added to Section 232 at 50%.

Section 232 of the Trade Expansion Act of 1962 allows the US president to impose tariffs based on national security concerns. The Department of Commerce conducts the underlying investigation. The Trump administration argues — and the Commerce reports support — that domestic steel, aluminium, and copper production capacity is insufficient for national defence requirements.

The first-term tariffs (2018-2020) hit steel at 25% and aluminium at 10%. The second-term escalation has been faster, broader, and at higher rates. The 50% rate on three primary metals is a meaningful departure from any prior US trade policy.

What the copper tariff actually covers

The Section 232 copper measure covers:

In scope (50% tariff): – Refined copper cathode (UNS C11000 and equivalent grades) – Copper anodes – Copper concentrate (if imported) – Copper alloys (including brass and bronze) – Copper wire rod – Copper bar and rod – Copper sheets and strip – Selected copper derivatives (motors, transformers, wire products)

Out of scope or under exception: – Copper scrap (case-by-case) – Specialty copper alloys used in semiconductor manufacturing (subject to review) – Some sub-categories of finished consumer electronics

The April 2026 overhaul significantly broadened the derivative product coverage — the original July 2025 measure focused on primary forms, while subsequent expansion drew in downstream products including household articles, certain automotive components, and selected industrial machinery containing copper. For 2025 trade flows, the immediate effect is on primary cathode imports.

What this does to US-bound copper trade flow

In 2024 the US consumed approximately 1.8 million MT of refined copper. Domestic production met roughly 50% of demand. The remainder was imported, primarily from:

Country | Approx 2024 imports (MT) | Share |

Chile | 540,000 | 30% |

Mexico | 270,000 | 15% |

Peru | 90,000 | 5% |

Canada | 90,000 | 5% |

Other (Australia, UAE, Kazakhstan, etc.) | 90,000 | 5% |

The 50% tariff applies to all of these origins. Chile retains a small advantage from the US-Chile Free Trade Agreement, but the Section 232 tariff supersedes most FTA preferences. The practical effect is a sharp landed-cost increase across all imported cathode.

US industrial buyers — electric motor manufacturers, cable producers, transformer assemblers — face three options:

- Pay the tariff. Absorb or pass through to end customers. This works for buyers with pricing power.

- Switch to scrap-based copper. Domestic copper scrap supplies a meaningful share of US recycled copper output. Scrap availability is limited by collection rates, but margins for scrap-based refiners have widened.

- Relocate downstream manufacturing. Producing finished products outside the US, then importing the finished goods if those products are not in the derivative tariff scope. This works for some products but the April 2026 expansion narrows that path.

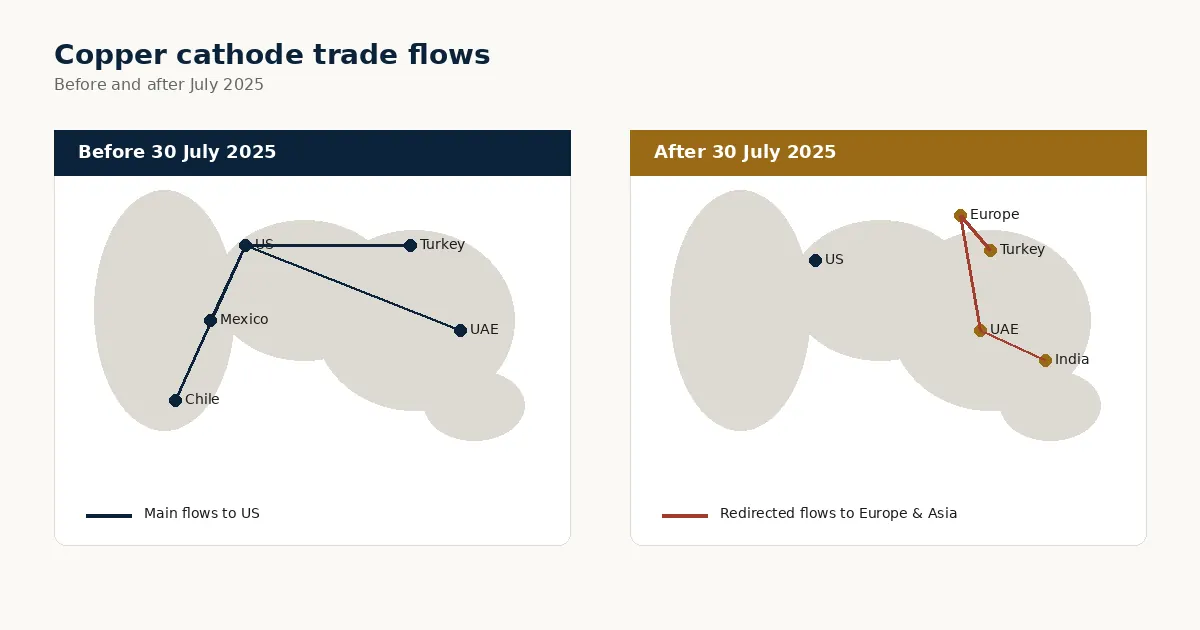

For Gulf cathode suppliers, the immediate effect is that US-bound shipments became uneconomic almost overnight. Au Club has not shipped material to US destinations since July 2025.

Arbitrage windows and where Gulf cathode is going instead

The displaced US demand creates space in Asian and European markets for cathode that would otherwise have moved west. Three trade flow shifts:

1. UAE/Turkey cathode → European premiums widening. With US-bound material now uneconomic, European buyers are competing harder for Gulf-sourced Grade A cathode. European cathode premium (the physical premium over LME) has widened by approximately $30-50/MT through Q3 2025.

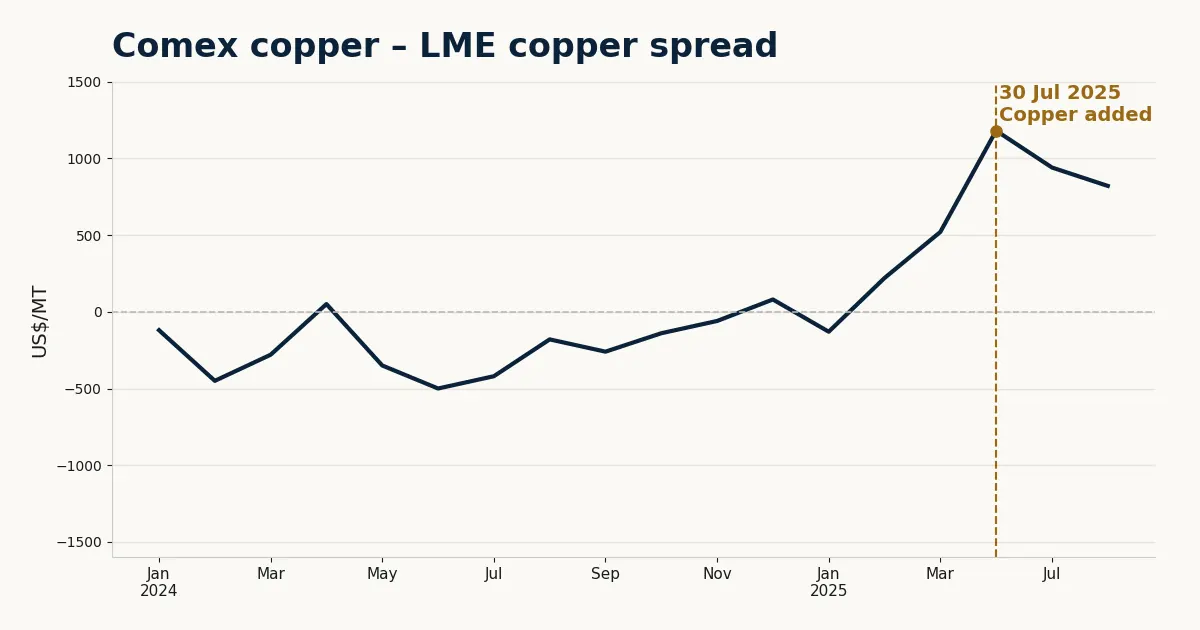

2. Comex-LME arbitrage. The Comex copper price (US domestic market) trades at a premium to LME (international market) approximately equal to the tariff cost. Traders who can move cathode through US customs at preferential rates (Free Trade Zone, USMCA where applicable) capture some of this spread. The arbitrage window has been wide in late 2025.

3. Asian cathode demand absorption. Chinese, Indian, and Southeast Asian buyers have absorbed some of the displaced US-bound volume. India in particular has expanded copper imports through 2025 as the country’s electrification programme accelerates.

For Au Club’s customer base, the practical effect: 2026 supply commitments are weighting toward Europe, India, Japan, and intra-Gulf delivery. US-nexus has effectively been removed from the working sales territory.

Compliance and documentation — what changes for cathode buyers

For non-US buyers, the documentation burden has increased even when they are not importing to the US. Three issues:

Smelter of origin documentation. Section 232 implementation references the country of last substantial transformation (typically the smelter location). Buyers re-exporting copper to the US — even from a third country — need clean smelter-of-origin documentation. Au Club provides this on every shipment.

Melt-and-pour records. Some Section 232 implementations have referenced “country of melt and pour” for steel and increasingly for copper. The COA, LME warrant, and smelter records together should establish this. Buyers should confirm their documentation package supports this attestation.

HTS code classification. Section 232 applies to specific HTS codes (Harmonized Tariff Schedule). Mis-classification — even unintentional — can result in penalties. Sophisticated US importers now use legal review of cathode HTS classifications before declaration.

What Au Club is writing into 2026 contracts

Three contract elements that have changed since July 2025:

Destination flexibility. Standard sales contracts now include explicit destination-change provisions allowing the buyer to divert cargo between approved destinations without penalty if tariff conditions change.

Tariff cost allocation. New contracts explicitly assign tariff cost to the buyer (DAP/DDP delivery to the destination) unless otherwise specified. CIF or FOB contracts naturally place tariff risk with the buyer, but customers have asked for explicit clauses.

Force majeure. Trade-policy actions (new tariffs, sanctions, export licence withdrawal at origin) are now explicitly listed as FM events. The generic FM language drafted before 2018 did not contemplate tariff regime changes.

Au Club’s read for 2026

Three working positions:

- The Section 232 copper tariff is permanent for the foreseeable future. It would take a meaningful US-China trade agreement or a change in administration to reverse. Neither is signalled for 2026.

- Gulf cathode flows shift permanently toward Asia and Europe. The US market is structurally less accessible for non-FTA cathode. UAE and Turkey will deepen Asian and European relationships.

- The Comex-LME spread will not fully close. Arbitrage compresses the spread but never eliminates it under a 50% tariff regime. Expect persistent premium for US-domestic copper.

For non-US cathode buyers, the picture is straightforwardly positive: more available supply, longer-tenor contracts on offer, and historically high — but stable — premium structures. For US buyers, the picture is challenging: paying for imported copper, competing for scrap, or relocating production.

FAQs

What is Section 232?

Section 232 of the Trade Expansion Act of 1962 allows the US president to impose tariffs on imports deemed a threat to national security. The Trump administration has used Section 232 for steel, aluminium, and (since 30 July 2025) copper at 50% rates.

Does Section 232 apply to copper scrap?

Currently scrap is largely out of scope or treated under exception, though this is subject to ongoing review.

How does Section 232 affect my non-US copper purchases?

If you are not importing to the US, the tariff does not directly apply. Indirectly, it has widened the spread between US (Comex) and international (LME) prices, and has shifted Gulf-origin cathode flows toward Asia and Europe.

Can the tariff be appealed or excluded?

The April 2026 overhaul eliminated most country-specific and product-specific exclusions that had accumulated. Some narrow exclusions remain available through Commerce Department review.

About Au Club

Au Club supplies LME Grade A copper cathode (99.99% Cu minimum) from Turkey and the UAE, primarily to European, Asian, and Gulf customers. Full smelter-of-origin documentation with each shipment. Multi-year supply structures available. Contact our trading desk to discuss your 2026 requirement.