VLSFO vs HSFO + Scrubber: A 2026 Total-Cost-of-Ownership Decision

Five years after IMO 2020, the scrubber decision is no longer about whether the technology works. It is about whether the HSFO-to-VLSFO price spread is wide enough to amortise the capital cost before the next regulato…

Five years after IMO 2020, the scrubber decision is no longer about whether the technology works. It is about whether the HSFO-to-VLSFO price spread is wide enough to amortise the capital cost before the next regulatory step changes the maths again. With MEPC 83 approving a carbon-pricing framework that takes effect on 1 March 2027, the answer for a vessel built around 2020-2021 has shifted from “obvious yes” to “depends on age, trade lane, and how aggressively you discount future carbon costs.” Here is the framework Au Club’s customers are using to make the 2026 decision.

What changed since IMO 2020 took effect

On 1 January 2020 the IMO’s 0.50% global sulphur cap entered force. Operators had three compliance options:

- Burn VLSFO (very low sulphur fuel oil) at 0.50% sulphur, or MGO/MDO

- Install a scrubber (Exhaust Gas Cleaning System, EGCS) and continue burning HSFO at 3.5% sulphur

- Switch to LNG, methanol, or another alternative fuel

Roughly 25% of the world fleet by tonnage installed scrubbers — disproportionately concentrated in container, tanker, and bulker segments where bunker is a high share of operating cost. Most of the remainder run on VLSFO.

The scrubber spread (the HSFO-to-VLSFO price differential) drove the economics. In early 2020 the spread averaged $250-300 per MT. With a typical scrubber capital cost of $4-8 million depending on vessel size, payback periods were one-to-three years for a modern Suezmax or VLCC.

Then the spread compressed.

The scrubber spread in 2020-2025

HSFO–VLSFO spread at Fujairah and Singapore, monthly averages

Period | Fujairah (/MT) | |

Q1 2020 | $290 | $310 |

Q1 2021 | $90 | $105 |

Q1 2022 | $145 | $160 |

Q1 2023 | $130 | $145 |

Q1 2024 | $110 | $125 |

Q1 2025 | $95 | $115 |

The compression was driven by two structural forces. Refineries adjusted their crude slate and product mix to produce more VLSFO. HSFO demand fell as part of the fleet converted permanently to VLSFO. The spread settled into a $80-130/MT range that has held for about three years.

At a $100/MT spread, a 200,000-MT-per-year bunker consumer saves $20 million per year by running HSFO + scrubber. That is still a meaningful number for a fleet operator. But at a $250/MT spread, the same operator was saving $50 million. The economics moved from “compelling” to “good.”

What the TCO model actually compares

A five-year total-cost-of-ownership comparison for a Suezmax tanker (modeled here as an illustrative working example, not specific operator economics):

Assumptions: – Vessel: Suezmax, 158,000 DWT – Annual bunker consumption: 14,000 MT – VLSFO price assumption: $580/MT – HSFO price assumption: $480/MT (spread $100/MT) – Scrubber capex (open-loop): $4 million, fully amortised over 5 years – Scrubber sludge disposal, NaOH (closed-loop only), and maintenance: $80,000/year per scrubber – MEPC 83 carbon-pricing impact phased in from March 2027 (so 2 years out of 5)

Five-year cumulative cost (USD millions)

Component | VLSFO | HSFO + open-loop scrubber | HSFO + closed-loop scrubber |

Bunker | $40.6 | $33.6 | $33.6 |

Scrubber capex | $0 | $4.0 | $5.5 |

Scrubber opex | $0 | $0.4 | $1.2 |

MEPC 83 carbon (2027-2029, estimated) | $1.8 | $2.6 | $2.6 |

Sludge + waste handling | $0 | $0.2 | $0.6 |

Total | $42.4 | $40.8 | $43.5 |

At a $100/MT spread, an open-loop scrubber breaks even or modestly outperforms VLSFO over five years on this profile. A closed-loop scrubber does not — the additional opex (sodium hydroxide for neutralisation, sludge disposal) offsets the bunker saving.

The number that matters is the spread. At $130/MT, open-loop wins comfortably. At $80/MT, it loses. Lock yourself into a regulatory environment that further raises HSFO’s emission cost (the MEPC 83 carbon factor) and the model tightens against scrubbers.

Operational realities the TCO model doesn’t capture

Three considerations that matter and are hard to quantify:

Open-loop discharge restrictions. Singapore prohibits open-loop scrubber discharge inside port limits. China’s coastal Emission Control Areas (Bohai, Yangtze River Delta, Pearl River Delta) restrict open-loop operation. The EU is debating tighter rules under FuelEU Maritime and revised port-state controls. Open-loop scrubbers are progressively losing operational windows. A vessel that spends 30% of its time in restricted waters loses 30% of the scrubber benefit on those legs.

Closed-loop opex. Closed-loop scrubbers do not discharge to sea, but they consume sodium hydroxide (caustic soda) and generate sludge that must be disposed of. NaOH consumption runs $50-150,000/year per vessel depending on operating profile. Sludge disposal at major ports varies; some ports charge $200-500/m³.

Resale value. A scrubber-fitted vessel commands a premium in the second-hand market when the spread is wide and a penalty when the spread is narrow. Predicting this five years out is genuinely difficult.

Carbon-pricing exposure. MEPC 83 prices Remedial Units at up to $380 per ton CO₂e above the base target by 2035. HSFO has a higher carbon factor than VLSFO (3.114 vs 3.151 — actually marginally lower per MT of fuel, because VLSFO has more carbon per MT). The well-to-wake intensity matters more than tank-to-wake under the IMO framework. Run the calculations with your bunker consumption and the framework’s intensity tables.

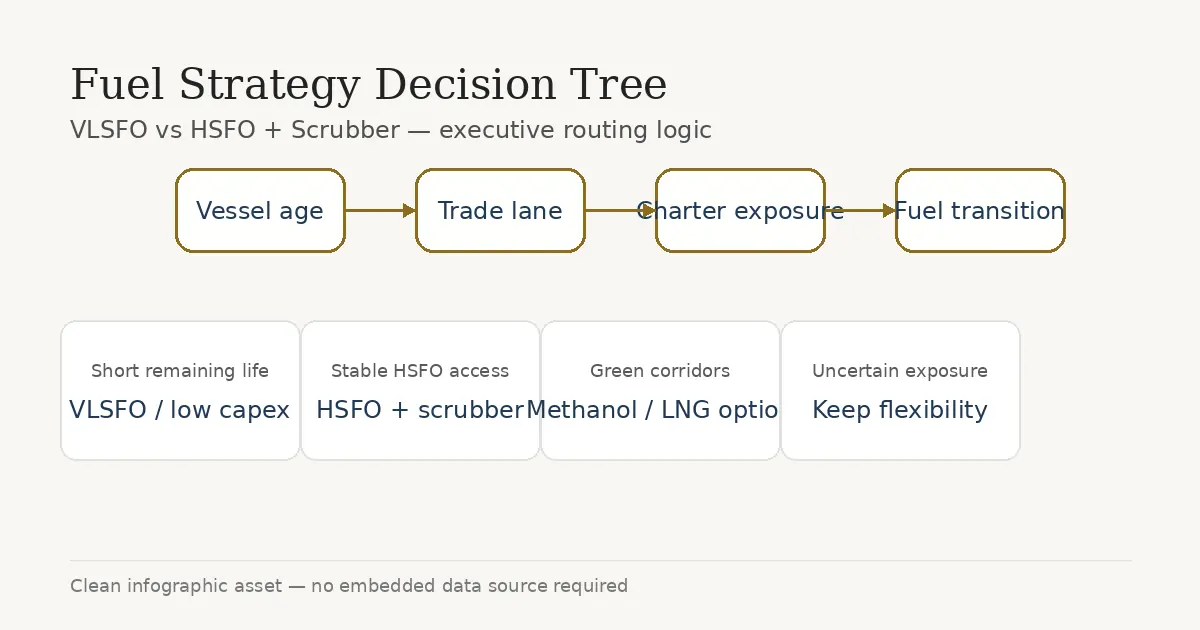

Decision tree for an owner or operator

Practical questions Au Club’s customers run through:

- Vessel age. If your vessel is under five years old and has fifteen years of trading life ahead, the capex amortisation works. If she has ten or fewer years left, payback windows are tight.

- Trade lane scrubber-friendliness. What share of your trading time is in open ocean vs in scrubber-restricted ports / ECAs? Open ocean tramping favours scrubbers. Asian intra-region container service does not.

- Charter market exposure. Are you trading on time charter (where the charterer pays bunkers) or on the spot market (where bunker cost is yours)? Spot market exposure makes the scrubber argument harder because spreads are unpredictable.

- Capital cost of capital. A high WACC penalises capex-heavy options. An owner with cheap debt sees scrubbers more favorably than one without.

- Future regulatory exposure. Lower-carbon fuels (LNG, methanol, biofuel) will further compress the scrubber economics over time. If you expect to convert to LNG within 7-10 years, do not install a scrubber now.

What we are telling fleet owners

Three working assumptions Au Club uses with customers in early 2025:

- Do not retrofit a scrubber to an existing VLSFO-burning vessel under 15 years old unless you have very specific circumstances. The capex payback period at current spreads is tight against further regulatory cost on HSFO.

- If you already have a scrubber, keep running it. Operating cost is meaningful but the capex is sunk. The five-year economics still work at $100/MT spread for most asset classes.

- For new-builds, evaluate LNG, methanol, and dual-fuel capability seriously. The 2027-2030 regulatory environment favours alternative fuels.

For mid-sized operators without inside views on refinery margins, the simplest rule is: lock VLSFO supply with a multi-year contract, monitor the scrubber spread monthly, and re-run the TCO model annually.

FAQs

What is the current HSFO-VLSFO spread at Fujairah?

As of Q1 2025, the spread is averaging around $95/MT. Contact our bunker desk for spot quotes.

Should I install a scrubber on a new-build vessel?

For most asset classes in 2025, no — the economics no longer support a 3-5 year payback at current spreads, and forward-looking carbon pricing further compresses the case. Evaluate LNG or methanol dual-fuel instead.

Are open-loop scrubbers banned?

Not globally. Singapore prohibits open-loop discharge inside port limits. China’s coastal ECAs restrict open-loop operation. The EU is reviewing rules. UAE waters currently allow open-loop discharge.

What does MEPC 83 do to my fuel cost?

The carbon-pricing framework enters force on 1 March 2027 and can add up to $380 per ton CO₂e by 2035 for fuel emissions above the base target. For a Suezmax burning VLSFO, that translates to a meaningful per-voyage cost. Au Club’s MEPC 83 article walks through worked examples.

About Au Club

Au Club supplies VLSFO (0.5% S) and HSFO (3.5% S) marine fuels at Jebel Ali, Port Khalifa, Fujairah, and Khor Fakkan. Multi-year supply contracts available. ISO 8217:2024 compliant. Contact our bunker desk to discuss your 2025-2026 bunker strategy.